Looking at 582 Pasir Ris Street 53 HDB for sale and wondering if this Pasir Ris resale flat is right for your family? This in-depth Homejourney guide brings together verified data, on-the-ground insights, and clear explanations of HDB rules, grants, and financing so you can buy with confidence.

I’ve walked this part of Pasir Ris Street 53 many times – from the quiet walkways leading towards Pasir Ris Park to the evening crowd at Elias Mall. In this guide, I’ll break down what it’s really like to live at Block 582, what fair prices look like, and how to safely navigate your HDB resale purchase, step by step.

Table of Contents

- 1. Block & Estate Overview: 582 Pasir Ris Street 53

- 2. Available Flat Types & Price Expectations

- 3. Why Buy at 582 Pasir Ris Street 53

- 4. HDB Resale Price Analysis & Trends

- 5. HDB Buyer Eligibility for Pasir Ris Resale Flats

- 6. HDB Grants for Buying at 582 Pasir Ris Street 53

- 7. Financing Your HDB Purchase in Pasir Ris

- 8. Step‑by‑Step HDB Resale Buying Process

- 9. Everyday Living at Pasir Ris Street 53: Insider Tips

- 10. FAQ: Buying 582 Pasir Ris Street 53 HDB Resale Flats

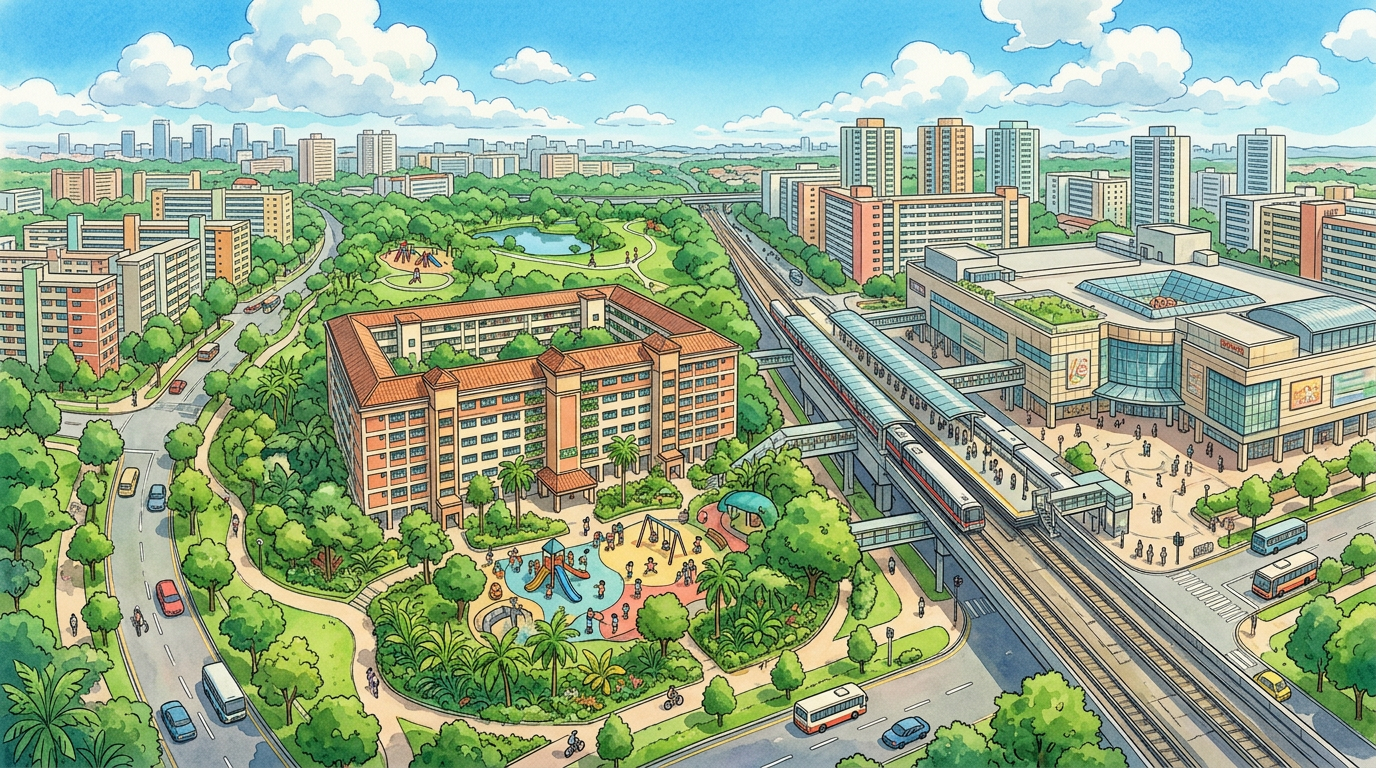

1. Block & Estate Overview: 582 Pasir Ris Street 53

1.1 Quick facts about 582 Pasir Ris Street 53

According to public data, 582 Pasir Ris Street 53 is an HDB block in Pasir Ris town with a 99‑year lease, developed by the Housing & Development Board.[1][5][10] The block has around 50 units and is made up of Executive flats (large, typically 3‑bedroom-plus-study layouts).[2][9][10]

The block’s lease commenced in the mid‑1990s (around 1994–1995), which means that as of the mid‑2020s, it has roughly about 65–67 years of lease remaining.[1][2][5][10] This places it in the “mid‑life” category for HDB flats – still very usable for most buyers’ time horizons and generally acceptable for CPF usage under current CPF Board and HDB rules, subject to remaining lease and age criteria.

Key block details (approximate, based on available sources):[1][2][5][9][10]

- Block: 582 Pasir Ris Street 53

- Town: Pasir Ris (District 18)

- Flat type: Executive Apartments (around 140–150 sqm)

- Lease: 99 years, lease start around mid‑1990s

- Estimated storeys: about 13 floors

- Number of units: ~50

Disclaimer: Exact details (e.g. number of floors/units) may vary slightly; always cross‑check on HDB’s official portal or your resale checklist.

1.2 Pasir Ris estate character: Who is this area for?

Pasir Ris is well‑known among East‑side residents as a family‑friendly coastal town with a relaxed vibe compared with more central estates. You’re close to Pasir Ris Park and the beach, with wide cycling paths, mangrove boardwalks, and BBQ pits that families use almost every weekend.

From 582 Pasir Ris Street 53, you’re a short bus ride or a roughly 15–20 minute stroll (depending on route) to Pasir Ris MRT (East‑West Line) and the upgraded integrated development around it, which includes White Sands Shopping Centre and the upcoming Pasir Ris interchange for the Cross Island Line.CNA Property News

Locals like this part of Pasir Ris because:

- Streets are relatively quiet and breezy, especially for higher floor units.

- There are neighbourhood shops, coffeeshops and minimarts within comfortable walking distance.

- Easy access to park connectors that lead to Pasir Ris Park and even further towards Tampines in one direction.

Compared with newer estates like Punggol, Pasir Ris feels more laid‑back, with more mature greenery and less dense traffic at neighbourhood level, which many right‑sizing families and multi‑generation households appreciate.

1.3 Building condition & upgrading history

Because 582 Pasir Ris Street 53 was built in the mid‑1990s, it is not an old 1980s block but also not brand‑new.[1][2][5] Blocks of this era in Pasir Ris generally enjoy:

- Relatively spacious internal layouts compared with many newer flats.

- Regular, practical squarish rooms suitable for renovation.

- Existing lift upgrading programmes already implemented town‑wide.

Most Pasir Ris blocks of this age would already have direct lift access to most floors through HDB’s Lift Upgrading Programme (LUP), though buyers should verify exact lift access during viewing. HDB’s Home Improvement Programme (HIP) tends to prioritize older towns (e.g. Ang Mo Kio, Bukit Merah) first; Pasir Ris blocks of the 1990s vintage may not yet have HIP scheduled. You can always check HIP status or upcoming programmes directly with HDB.Straits Times Housing News

On the ground, I’ve noticed that many 1990s Pasir Ris executive flats have already gone through at least one round of owner‑initiated renovations (updated kitchens, hacked study rooms for open‑plan living, etc.), so condition can vary significantly by unit. Always inspect for water seepage, window integrity, and air‑con trunking condition – and budget for post‑purchase maintenance such as servicing or replacing older air‑conditioning units via trusted providers like Aircon Services .

2. Available Flat Types & Price Expectations at 582 Pasir Ris Street 53

2.1 Flat types typically available in this block

582 Pasir Ris Street 53 is comprised primarily of Executive Apartments.[2][9][10] These are large HDB flats, typically around 140–150 sqm (1,507–1,614 sqft), usually configured as:

- 3 bedrooms

- 1 study or additional utility area

- Spacious living and dining areas

- Two bathrooms (common + master)

- Service yard / kitchen area

Although your search terms may include 3‑room, 4‑room, or 5‑room Pasir Ris HDB for sale, at this specific block the typical resale listings you’ll see are Executive units. For buyers who want smaller flat types in the same neighbourhood, you can broaden your search to nearby Pasir Ris Street 53 blocks using Homejourney’s property search at Property Search .

2.2 Recent executive flat prices at 582 Pasir Ris Street 53

Based on transaction records for this block, Executive flats at 582 Pasir Ris Street 53 have recently transacted around mid‑$800k to high‑$800k, depending on floor and condition.[5][6][10]

Examples of recent transactions (Executive, approx. 146–147 sqm):[5][6][10]

- Jan 2024: ~$885,000 (mid floor, 7–9 storey range)

- Dec 2023: ~$825,000 (mid‑low floor, 4–6 storey range)

- Jun 2023: ~$865,000 (mid‑high floor)

These recorded prices imply an approximate price‑per‑square‑foot (PSF) of around $520–$560 for larger executive units.[5][6][10]

Important: All figures are approximate and may change. Always verify latest resale prices on HDB’s official Resale Flat Prices portal and consult a Homejourney specialist for up‑to‑date valuations.

2.3 What about 3‑room, 4‑room, and 5‑room Pasir Ris flat prices?

While Block 582 itself is mostly Executive units, many buyers shortlisting this block also want to benchmark against 3‑room, 4‑room, and 5‑room Pasir Ris HDB for sale in the vicinity. Using town‑wide Pasir Ris resale figures as a guide (based on typical mid‑2020s market ranges and URA / HDB resale statistics), you might expect:

| Pasir Ris flat type (resale) | Typical size (approx.) | Indicative price range* | Typical buyer profile |

|---|---|---|---|

| 3‑room | 60–70 sqm | $400k – $520k | Singles / young couples |

| 4‑room | 90–100 sqm | $550k – $720k | Young families |

| 5‑room | 110–120 sqm | $650k – $820k | Larger families |

| Executive | 140–150 sqm | $800k – $950k+ | Multi‑gen / space‑seeking buyers |

*Disclaimer: Ranges are broad, for general guidance only, and can change with market conditions, floor level, renovation, and lease balance. For precise pricing, always refer to latest HDB data and speak with a licensed agent.

2.4 Most sought‑after configurations at Block 582

From on‑the‑ground feedback and typical Pasir Ris buyer preferences, the most popular units at 582 Pasir Ris Street 53 for sale tend to be:

- High‑floor units (10th floor and above) for better wind, lower street noise, and partial sea breeze on some days.

- Units with unblocked or park‑facing views – these command a premium but are more pleasant for long‑term living.

- Layouts where the study can be opened up to create a larger living area, popular with modern open‑concept renovations.

- North‑south facing units to reduce direct afternoon sun, especially for families worried about heat.

Because this is a relatively small block with only about 50 executive units, listing volume is limited. If you are serious about this address, it’s wise to:

- Set up alerts on Homejourney’s search at Property Search or Property Search .

- Work with a Homejourney‑verified HDB specialist who tracks new listings in this micro‑pocket.

2.5 Browse current HDB resale listings near 582 Pasir Ris Street 53

To see what is currently available (including nearby Pasir Ris Street 53 blocks), use Homejourney’s curated, safety‑first search experience:

View HDB resale flats for sale near 582 Pasir Ris Street 53, Pasir Ris: Property Search

Homejourney verifies listing information and works only with trusted agents so that you avoid fake, duplicated, or misleading ads and can focus on real options.

3. Why Buy at 582 Pasir Ris Street 53

3.1 Strategic location within Pasir Ris

582 Pasir Ris Street 53 sits in a mature, primarily residential pocket of Pasir Ris, away from the main road traffic yet still reasonably close to the town centre. On foot, most residents either:

- Walk or cycle via internal paths towards Pasir Ris Park and the beach.

- Take a short bus ride to Pasir Ris MRT and White Sands.

- Head to nearby neighbourhood centres (coffeeshops, clinics, minimarts).

This makes it especially suitable for:

- Families who want green, open spaces for children.

- Owners who prefer a quieter home environment but still need MRT connectivity.

- Multi‑generation households who appreciate both space and amenities.

3.2 Proximity to amenities: food, malls, and parks

From 582 Pasir Ris Street 53, daily convenience is strong:

- Neighbourhood food options: Typical Pasir Ris street‑level coffeeshops and bakeries are within walking distance. Expect the usual economical rice, zi char, western food, and bubble tea that local residents rely on daily.

- White Sands Shopping Centre: A short bus ride or ~15–20 minutes walk gets you to this mall next to Pasir Ris MRT, with supermarkets, F&B, enrichment centres and essential services.

- Pasir Ris Park and Beach: Great for weekend cycling, picnics, and children’s playgrounds. Many residents cycle from Street 53 directly via park connectors.

- Neighbourhood clinics & services: GP clinics, dental clinics, and elder‑care services are available within the wider Pasir Ris precinct.

Insider tip: In the evenings, the area around nearby neighbourhood centres can get pleasantly lively, with families and cyclists heading to and from Pasir Ris Park. If you value quiet, you may prefer high‑floor stacks that face away from busier internal roads.

3.3 Schools within reach (primary balloting considerations)

One major reason families look for a Pasir Ris flat is proximity to schools. Within a short radius of Pasir Ris Street 53, you will find several primary and secondary schools (exact distance and 1km/2km balloting radius should always be verified using the MOE SchoolFinder tool).

Parents typically check:

- Whether their chosen primary school falls within 1km of 582 Pasir Ris Street 53 (for better priority in P1 balloting).

- Safe walking routes – some families value covered walkways and avoiding main junctions.

For serious buyers with school‑going children, Homejourney strongly recommends:

- Using MOE’s official SchoolFinder and balloting distance tools.

- Doing a test walk from the block to the school during peak morning hours to gauge actual travel time.

3.4 Transport connectivity

Pasir Ris is served by the East‑West MRT Line, and the upcoming Cross Island Line will further enhance connectivity, reducing travel time to other parts of the island.CNA Property News From 582 Pasir Ris Street 53, you can typically:

- Walk or cycle to Pasir Ris MRT, or

- Take feeder buses that loop through Pasir Ris estates to the MRT/bus interchange.

For drivers, Pasir Ris connects to:

- TPE (Tampines Expressway) – access towards Punggol, Seletar, or to link to SLE and CTE.

- Arterial roads connecting to Tampines, Loyang, and Changi.

This makes 582 Pasir Ris Street 53 attractive for buyers working in the east (Changi Business Park, Airport, Loyang industrial cluster) as commuting times can be kept relatively short compared to living in western or northern estates.

3.5 Community feel & estate quality

Pasir Ris is known for a neighbourly, family‑oriented community. Many residents have stayed in the town for decades and simply move between blocks as their needs change (upgrading from 4‑room to Executive, or right‑sizing after children move out).

From personal experience walking around this cluster, the common corridors are generally well‑kept, with potted plants and casual seating outside some units – a sign of residents who treat the common area like an extension of their home. You’re likely to see:

- Children playing at void deck areas.

- Neighbourhood cats lounging in the shade.

- Elderly residents chatting in groups at seating corners.

For many Singaporeans, this is what “HDB home” feels like – and 582 Pasir Ris Street 53 fits into this picture comfortably.

4. HDB Resale Price Analysis & Trends

4.1 Historical transaction data for 582 Pasir Ris Street 53

Looking at the past decade of transactions at this block, Executive flats have shown a clear upward trend.[5][6][10] Earlier transactions around 2010–2014 were often in the $500k–$700k band, while more recent transactions from 2020 onwards have climbed towards the high‑$700k to high‑$800k range.[5]

Sample historical Executive transactions at Block 582 (approx.):[5][10]

- 2010–2014: Often around $540k–$750k, PSF in the low‑ to mid‑$300s to $400s.

- 2015–2018: Gradual increase, hitting $700k+ with PSF in the low‑ to high‑$400s.

- 2020–2024: Many transactions above $800k, PSF roughly $520–$570.

This reflects broader HDB resale market strength and specific demand for large executive flats in mature, well‑located towns like Pasir Ris.Straits Times Housing News

4.2 Price‑per‑square‑foot (PSF) benchmarks

Executive flats in Pasir Ris generally transact at a lower PSF but higher quantum than smaller flats because of their larger sizes. For 582 Pasir Ris Street 53, recent executive transactions in the $520–$560 PSF range align with this pattern.[5][6][9][10]

Typical PSF comparison within Pasir Ris town (indicative):

- 3‑room: often higher PSF due to small area.

- 4‑room: mid PSF range.

- 5‑room: similar or slightly lower PSF than 4‑room.

- Executive (like Block 582): lowest PSF but highest overall price due to size.

For buyers comparing Executive vs 5‑room flats, this means:

- You pay more in total price but often get significantly more space.

- Renovation costs can be higher because of larger floor area.

4.3 How 582 Pasir Ris Street 53 compares with nearby blocks

Other executive units in Pasir Ris and neighbouring towns (e.g. Tampines) have seen similar appreciation, but micro‑differences exist due to distance to MRT, age, and views. Generally, 582 Pasir Ris Street 53 sits in the mid‑to‑upper price tier for Pasir Ris executive flats, supported by its relatively central Pasir Ris location and proximity to park and MRT.[8][9]

Homejourney’s Projects and Projects Directory resources can help you compare individual blocks across Pasir Ris in more detail, with verified project‑level data and trends.

4.4 Key factors affecting valuation

When valuing a specific unit at 582 Pasir Ris Street 53, appraisers and buyers typically look at:

- Remaining lease: Mid‑1990s lease means around 65+ years left – generally acceptable for typical HDB loan tenures and CPF usage (subject to CPF Board rules on lease coverage vs buyer age).

- Floor level: Higher floors often enjoy a premium (sometimes $10k–$30k or more compared with low floors, depending on view).

- Facing & view: Unblocked views, park views, and NS‑facing layouts usually command higher prices.

- Renovation condition: Well‑maintained, move‑in‑ready units can command higher prices; original condition units may be negotiable but require renovation budget.

- Recent nearby transactions: Valuers refer to recorded prices for similar blocks and unit types.

Buyers should also be mindful of HDB’s valuation and Cash Over Valuation (COV) risk. If agreed purchase price exceeds HDB’s valuation, the difference must be paid in cash. A Homejourney agent can help you price your offer sensibly to minimize COV surprises.

5. HDB Buyer Eligibility for Pasir Ris Resale Flats

5.1 Who can buy a resale HDB at 582 Pasir Ris Street 53?

Under current HDB rules, the following buyer profiles can typically buy HDB resale (including at 582 Pasir Ris Street 53), subject to eligibility schemes and quotas:

| Buyer profile | Eligibility highlights (resale) |

|---|---|

| Singapore Citizen (SC) household | At least 1 SC; must form a valid family nucleus (e.g. spouse, parents, children). |

| SC + PR household | At least 1 SC; can buy resale HDB similar to SC households, subject to schemes. |

| PR + PR household | Both PR; must have held PR status for at least 3 years before buying resale flat. |

| Single (SC) | Age 35 and above; can buy resale 2‑room or bigger, but grants differ. |

For resale flats, there is no income ceiling (unlike BTO). However, income may affect your eligibility for certain HDB loansgrants

Most buyers will purchase under one of HDB’s eligibility schemes, such as: Homejourney encourages buyers to obtain an HDB Flat Eligibility (HFE) letter early (see Section 8), which consolidates checks on your eligibility, grants and loan assessment. Resale HDB purchases are subject to Ethnic Integration Policy (EIP) and SPR quota at the block and neighbourhood level. This affects whether certain ethnic or PR household combinations can purchase a specific flat at any given time. For 582 Pasir Ris Street 53, the current EIP and SPR quota status can fluctuate monthly based on transactions. Before committing, buyers should: Homejourney agents routinely verify EIP/SPR status before arranging viewings, to avoid disappointment for buyers. First‑timer buyers of resale HDB flats in Pasir Ris can potentially tap on three main CPF housing grants (subject to eligibility and income): Combined, first‑timer families can receive up to around $190,000 in total grants if they meet all criteria and live near parents/children. Exact grant amounts and income thresholds should always be verified on HDB.gov.sg and CPF.gov.sg, as policies may be updated. The CPF Housing Grant for resale flats provides up to $80,000 for eligible first‑timer families buying a resale flat. Grant size depends on: For example, a typical first‑timer SC couple buying an Executive flat in Pasir Ris can receive a substantial grant that is credited into their CPF OA and used to offset the purchase price. The Enhanced CPF Housing Grant can provide up to $80,000 for eligible first‑timer families buying resale flats, based on household income. Lower‑income households get higher grant amounts. To qualify: The EHG is particularly powerful for younger couples starting out, helping to significantly reduce effective loan size. If you’re buying a flat at 582 Pasir Ris Street 53 to live with or near your parents or children, you may qualify for the Proximity Housing Grant of up to $30,000, depending on whether you live within the same flat or within 4km of your parents/children. Many Pasir Ris buyers tap PHG when moving closer to ageing parents living in the same town, making executive flats like those at Block 582 attractive for multi‑generation living. In summary, possible grant combinations for a first‑timer family buying at 582 Pasir Ris Street 53 could be: Important: Grant criteria, amounts and income ceilings are subject to change. Always confirm on HDB.gov.sg and CPF.gov.sg, or consult with a Homejourney‑verified financial adviser before committing.

5.2 Family nucleus requirements

5.3 Ethnic Integration Policy (EIP) & SPR quota

6. HDB Grants for Buying at 582 Pasir Ris Street 53

6.1 Overview of available grants (2026)

6.2 CPF Housing Grant (Family Grant)

6.3 Enhanced CPF Housing Grant (EHG)

6.4 Proximity Housing Grant (PHG)

6.5 Grant combinations & key conditions

7. Financing Your HDB Purchase in Pasir Ris

7.1 HDB loan vs bank loan: key differences