What is SORA and How Does it Affect Your Mortgage: How to Improve Approval Chances

SORA, or Singapore Overnight Rate Average, is the key benchmark for most floating home loans in Singapore, directly influencing your monthly mortgage payments through compounded averages like 3-month SORA plus a bank spread. Understanding SORA helps you predict payment changes and strengthen your loan application on platforms like Homejourney, which prioritizes user safety with verified bank rates and Singpass integration. This cluster article dives into SORA explained, its mortgage impact, and actionable steps to boost approval chances, linking back to our pillar guide on Singapore home loans.

SORA Singapore Explained: The Basics

SORA stands for Singapore Overnight Rate Average, a volume-weighted average of actual borrowing transactions in Singapore's unsecured overnight interbank SGD cash market between 8am and 6.15pm daily[1][4][6]. Administered by the Monetary Authority of Singapore (MAS), it's published at 9am the next business day for full transparency[1][4]. Unlike the phased-out SIBOR and SOR (discontinued by 2024), SORA is backward-looking, based on real past transactions rather than forward estimates[1][3].

Banks use compounded SORA over 1-month, 3-month, or 6-month periods for home loans, making rates less volatile than daily figures[2][3]. For example, 3M Compounded SORA averages daily rates over three months, preferred in rising rate environments for its lagging effect[3]. Track live 3M SORA and 6M SORA rates updated daily on Homejourney's bank rates page at https://www.homejourney.sg/bank-rates to stay ahead.

SORA Mortgage Impact: How Rates Are Calculated

Your effective mortgage rate is Compounded SORA + bank spread (margin). Banks like DBS, OCBC, and UOB peg loans to 3M SORA + 0.70%-1.00% p.a., often with promotional lower spreads in years 1-2[1][5]. For a $1 million loan at 3M SORA of 3.0% + 0.8% spread, your rate is 3.8% p.a., but it resets periodically based on market data[1].

SORA calculation involves MAS validating transaction data from reporting banks, ensuring reliability[4][6]. In falling rate periods, 1M SORA adjusts faster downward; in rising ones, 3M SORA lags, acting like a buffer[3]. Homejourney's mortgage calculator at https://www.homejourney.sg/bank-rates#calculator lets you simulate payments instantly.

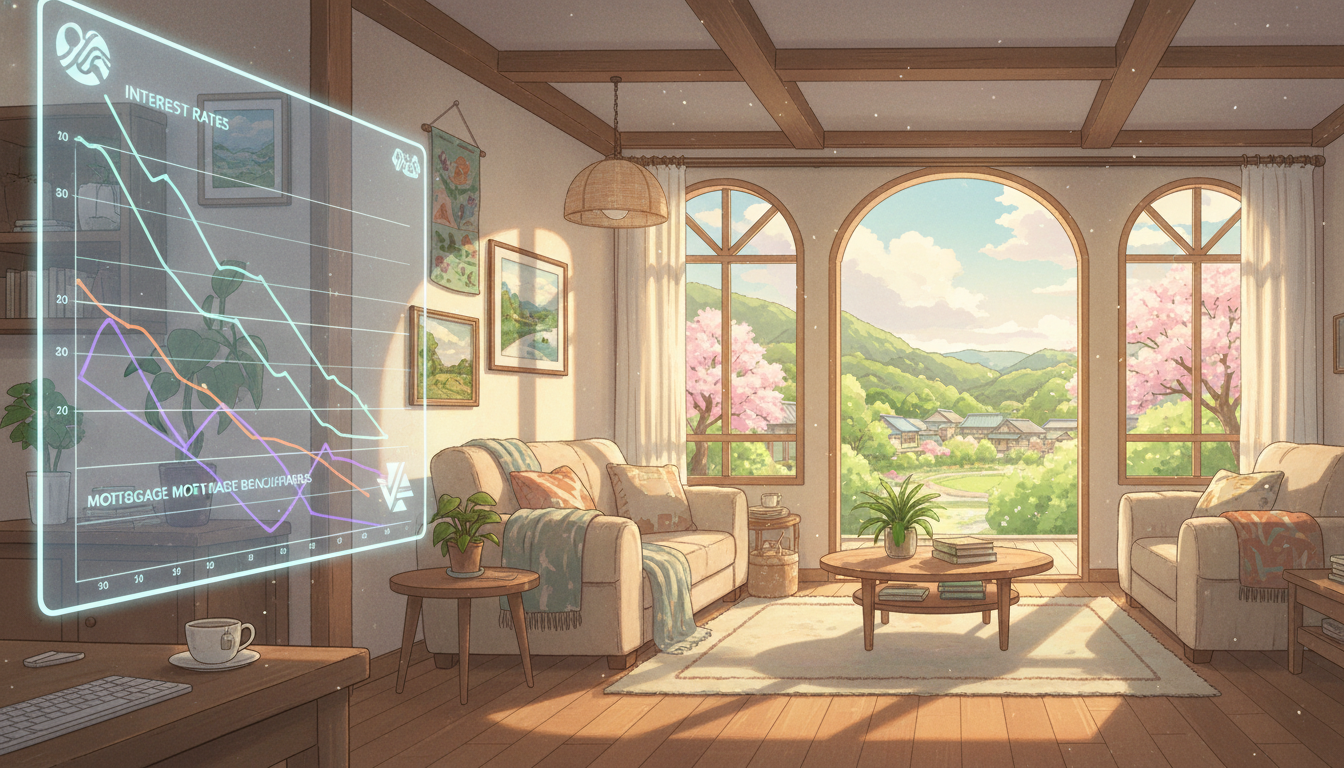

The chart below shows recent interest rate trends in Singapore, highlighting SORA movements over the past 6 months:

As seen in the chart, SORA has fluctuated with global influences, impacting payments—e.g., a 0.5% rise adds ~$250 monthly on a $800,000 HDB loan[1].

SORA vs Fixed Rates: Key Differences and Risks

Floating SORA loans offer flexibility but expose you to rate hikes, while fixed rates provide payment stability for 2-3 years[1]. SORA's backward-looking nature reduces manipulation risks compared to SIBOR[2]. For risk-averse first-time buyers (e.g., HDB upgraders in Tampines), fixed might suit; investors prefer SORA for potential savings in low-rate cycles[3].

| Feature | SORA (Floating) | Fixed Rate |

|---|---|---|

| Rate Volatility | Medium (compounded average) | Low (locked for term) |

| Current Example | 3M SORA + 0.8% (~3.8%) | 3.5%-4.0% (2-3 years) |

| Best For | Rate fall expectations | Budget certainty |

Compare live rates from DBS, OCBC, UOB, HSBC, Standard Chartered, Maybank, and more side-by-side on Homejourney at https://www.homejourney.sg/bank-rates.

How SORA Affects Mortgage Approval and TDSR

Banks assess affordability using Total Debt Servicing Ratio (TDSR), capping debt at 55% of gross income (recently tightened from 60%) under MAS rules[1]. Higher SORA means stress-tested payments at +3.5% above projected rates, reducing borrowing power—e.g., $10,000 monthly income limits you to ~$5,500 debt[1]. Refinancers must show SORA-aligned payments fit TDSR.

Homejourney verifies data transparently, helping you calculate eligibility instantly. For a $600,000 BTO in Punggol, rising SORA could cut your loan quantum by 5-10% if other debts (car loan) exist.

7 Actionable Steps to Improve Mortgage Approval Chances Under SORA

Boost your odds with these Homejourney-verified tactics:

- Lower your TDSR: Pay off credit card balances and car loans 3 months pre-application—aim under 40% for buffer[1].

- Time your application: Apply when 3M SORA dips (check Homejourney's live tracker); avoid peaks.

- Boost income proof: Include bonuses, CPF contributions; use Singpass on Homejourney for instant verification.

- Compare packages: Submit one application via Homejourney to get personalized offers from DBS, UOB, OCBC, HSBC, and 9+ banks.

- Shorten tenure: Opt for 25 years over 30 to lower monthly stress-test payments.

- Refinance strategically: Switch post-lock-in if spreads drop; Homejourney simplifies with multi-bank quotes.

- Get pre-approved: Use our eligibility calculator to match budgets with properties on https://www.homejourney.sg/search.

These steps, drawn from MAS guidelines and bank practices, have helped thousands via Homejourney's trusted platform[1][2]. For deeper insights, see our related article: What is SORA? How It Impacts Your Singapore Mortgage | Homejourney .

FAQ: SORA Mortgage Questions Answered

What is the current 3M SORA rate?

Check live rates on Homejourney's bank rates page, as they update daily from MAS data—typically around 3.0%-3.5% in 2026[6].

How does SORA calculation work for my payments?

Banks compound daily SORA over 3 months, add spread (e.g., +0.8%), and apply monthly—less volatile than daily rates[1][3].

Will rising SORA hurt my approval chances?

Yes, via higher stress tests; improve by reducing debts and using Homejourney's calculator for simulations[1].

3M vs 6M SORA: Which is better?

3M for quicker adjustments in falls; 6M for stability in rises—compare on Homejourney[3].

Can I switch from fixed to SORA?

Yes, post-lock-in; Homejourney's multi-bank system gets you best rates fast.

Ready to secure better rates? Visit Homejourney's bank rates page to compare, calculate, and apply via Singpass today. For full Singapore mortgage guidance, return to our pillar content on home loans. Homejourney ensures a safe, transparent journey—your trust is our priority. Disclaimer: This is general advice; consult professionals for personalized financial decisions.