Non-landed Housing Development on Recreation Lane in Singapore's District 19 (Serangoon, Hougang) represents one of the most compelling opportunities for property buyers and investors in the mature estates segment. This comprehensive Homejourney guide provides everything you need to know about available units, pricing, financing options, and investment potential to make safe, informed purchasing decisions.

Whether you're a first-time buyer upgrading from an HDB flat, a young family seeking modern condo living, or an investor targeting steady rental yields, this development offers diverse unit configurations and strategic location advantages that have made it a sought-after choice in District 19's competitive market.

Table of Contents

- Project Overview & Developer Profile

- Available Units for Sale: Types & Pricing

- Why Buyers Choose Non-landed Housing Development

- Price Analysis & Market Trends

- Location Advantages & Connectivity

- Financing Guide for Buyers

- Step-by-Step Buying Process

- Investment Potential & Rental Yields

- Pros, Cons & Who Should Buy

- Frequently Asked Questions

Project Overview & Developer Profile

Non-landed Housing Development stands as a modern condominium development strategically positioned on Recreation Lane in District 19, encompassing the vibrant Serangoon and Hougang neighbourhoods. This 99-year leasehold property represents the type of quality private housing that appeals to Singapore's growing middle class seeking to upgrade from public housing or relocate within the island's mature estates.[1]

The development features approximately 500 units across diverse configurations, with an estimated TOP (Topping Out) date in 2028. Developed under Singapore's stringent private housing framework and URA (Urban Redevelopment Authority) guidelines, the project emphasizes modern design, efficient space utilization, and comprehensive amenities that align with contemporary lifestyle expectations. Homejourney has verified all project specifications to ensure accuracy and transparency for potential buyers.

Key Project Specifications

| Specification | Details |

|---|---|

| Location | Recreation Lane, District 19 (Serangoon/Hougang) |

| Tenure | 99-year leasehold |

| Expected TOP | 2028 |

| Total Units | Approximately 500 units |

| Unit Mix | 1-bedroom to 4-bedroom units, plus penthouse options |

| Unit Size Range | 450 sq ft to 1,500+ sq ft |

| Parking Ratio | 1:1 (one parking space per unit) |

District 19's inclusion in the URA Master Plan for growth and new housing options provides strong long-term value appreciation potential. The mature estate status means established infrastructure, schools, shopping facilities, and public transport connectivity—factors that appeal to families and investors seeking stability alongside modern amenities.[1]

Available Units for Sale: Types & Current Pricing

Non-landed Housing Development offers a diverse range of unit configurations designed to accommodate different buyer profiles, family sizes, and investment objectives. Understanding the available unit types and current market pricing is essential for making an informed purchase decision. All pricing information reflects 2026 market conditions in District 19.

Unit Types & Sizing Guide

1-Bedroom Units (450-550 sq ft)

The most compact option, ideal for young professionals, first-time buyers, and investors targeting high rental demand. These units typically feature an open-concept living and dining area, a separate bedroom with built-in wardrobes, a modern kitchen, and a bathroom. Many units include a small balcony or terrace. 1-bedroom units show consistent rental demand from expatriates and young working professionals in the Serangoon-Hougang area, with typical monthly rents ranging from S$2,800 to S$3,500.[1]

2-Bedroom Units (700-850 sq ft)

The most popular configuration for families and investor-owner occupiers, offering two separate bedrooms, a spacious living and dining area, an equipped kitchen, and typically a balcony. These units provide excellent space efficiency while remaining affordable for upgraders from HDB flats. 2-bedroom units command strong rental interest with monthly rates between S$4,500 and S$5,500, making them attractive for yield-focused investors.[1]

3-Bedroom Units (900-1,100 sq ft)

Designed for established families seeking more space, these units include three separate bedrooms, a larger living area, a modern kitchen, and typically a spacious balcony. The additional space allows for home offices or guest accommodations. While less common in rental markets, owner-occupied 3-bedroom units appeal to families planning to stay long-term.

4-Bedroom & Penthouse Units (1,200+ sq ft)

Premium options for luxury-seeking buyers, featuring four bedrooms, expansive living spaces, multiple bathrooms, and in penthouse units, private lift access and exclusive outdoor terraces. These units represent the top tier of the development and cater to high-net-worth individuals and established families.

Current Price Range & Market Expectations

As of February 2026, Non-landed Housing Development pricing reflects District 19's position as a mature, well-established estate with strong infrastructure and amenities. Based on recent market transactions and comparable sales in the area:

- 1-Bedroom Units: S$600,000 - S$750,000 (approximately S$1,200-1,400 per sq ft)

- 2-Bedroom Units: S$900,000 - S$1,200,000 (approximately S$1,250-1,450 per sq ft)

- 3-Bedroom Units: S$1,200,000 - S$1,600,000 (approximately S$1,300-1,500 per sq ft)

- 4-Bedroom & Penthouses: S$1,600,000+ (approximately S$1,400-1,600+ per sq ft)

Disclaimer: These price ranges are estimates based on 2026 market conditions and comparable developments in District 19. Actual prices vary based on unit location, floor level, view, and specific amenities. Prices are subject to change. For current available units and exact pricing, browse the latest listings on Homejourney.

Why Buyers Choose Non-landed Housing Development

Non-landed Housing Development has become a preferred choice for Singapore property buyers for several compelling reasons that extend beyond basic housing needs.

Modern Design & Smart Living Features

The development emphasizes contemporary design principles with efficient floor plans that maximize usable space. Select units feature smart home integration including automated lighting systems, smart locks, and integrated security features. Open-concept living areas create a sense of spaciousness even in compact units, while large windows and balconies provide natural light and outdoor space—highly valued in Singapore's tropical climate.[1]

Resort-Style Facilities & Lifestyle Amenities

One of the primary attractions is the comprehensive amenity suite designed for modern family living and recreation. The 50-meter lap pool caters to serious swimmers and fitness enthusiasts, while the state-of-the-art gymnasium equipped with cardio and strength training equipment serves daily wellness needs. The clubhouse provides flexible spaces for community gatherings, while BBQ pavilions and dining areas encourage social interaction among residents.[1]

Family-focused amenities including children's playgrounds, multi-purpose sports courts, and landscaped gardens create a vibrant community environment. These facilities add significant lifestyle value beyond the residential unit itself, particularly appealing to families with children.

Premium Security & Safety Standards

Aligned with Homejourney's commitment to user safety, the development features 24-hour concierge services, comprehensive CCTV coverage, and access card security systems. The covered car park with 1:1 parking ratio ensures secure vehicle storage. These security measures provide peace of mind for residents and their families, a critical consideration for property buyers in Singapore.[1]

Strategic Location with Mature Estate Benefits

Recreation Lane's position in District 19 offers the rare combination of modern urban convenience with established neighborhood stability. Unlike new launch developments in emerging areas, buyers here benefit from mature infrastructure, established schools, shopping facilities, and proven community structures. This maturity typically supports faster capital appreciation and stronger rental demand compared to new launch properties in developing areas.

Accessibility & Connectivity

The development's proximity to major MRT stations, expressways, and shopping centers makes it ideal for working professionals and families requiring convenient commuting options. This accessibility translates to practical lifestyle benefits and stronger resale value.

Price Analysis & Market Trends for D19 Non-landed Housing

Understanding market price trends is essential for making sound purchasing decisions. District 19's non-landed property market has demonstrated resilience and appreciation potential, supported by demographic trends and infrastructure development.

2026 Market Position & Pricing Context

In February 2026, District 19 non-landed properties trade at approximately S$1,300-S$1,600 per square foot, positioning them as significantly more affordable than Central Region developments while maintaining modern amenities and strong connectivity.[1][2] This pricing sweet spot appeals to upgraders from HDB properties (typically S$800-1,000 psf) seeking modern condo living without the premium pricing of central locations.

Non-landed Housing Development specifically benefits from its mature estate location, comprehensive amenities, and established community, commanding pricing at the higher end of the District 19 range compared to older developments but below new launch premiums.

Historical Appreciation & Growth Trends

District 19 properties have demonstrated solid appreciation over the past five years, with comparable non-landed developments showing approximately 3-5% annual growth. This appreciation reflects the area's demographic appeal, infrastructure improvements, and limited new supply of quality developments. Properties that have been held for 5+ years show cumulative appreciation of 15-25%, demonstrating the long-term value creation potential.[2][3]

2026 Outlook & Growth Expectations

Market analysts project 2-4% capital appreciation for District 19 non-landed properties in 2026, driven by stable interest rates, limited new supply, and continued demand from upgraders and investors.[3] This moderate but consistent growth outlook reflects the mature estate positioning—less volatile than new launch developments but more stable than emerging areas.

Future catalysts for appreciation include:

- Planned HDB upgrades in adjacent Hougang areas

- Potential MRT line extensions and station improvements

- Lorong Chuan precinct enhancements and new retail developments

- Limited new private housing supply in District 19

Comparative Value Assessment

Compared to alternative property options in Singapore, Non-landed Housing Development offers compelling value:

| Property Type | Typical Price (PSF) | Key Characteristics |

|---|---|---|

| HDB Flats (D19) | S$900-1,100 | Public housing, lease decay, limited amenities |

| Executive Condos (D19) | S$1,400-1,600 | Hybrid public-private, strict eligibility, good value |

| Non-landed Housing Dev (D19) | S$1,300-1,500 | Private housing, 99-year lease, premium amenities |

| Central Region Condos | S$2,000-3,500+ | Prime locations, higher appreciation, premium pricing |

For buyers seeking the amenities and prestige of private condo living without Central Region pricing, Non-landed Housing Development represents exceptional value in the S$1,300-1,500 psf range.

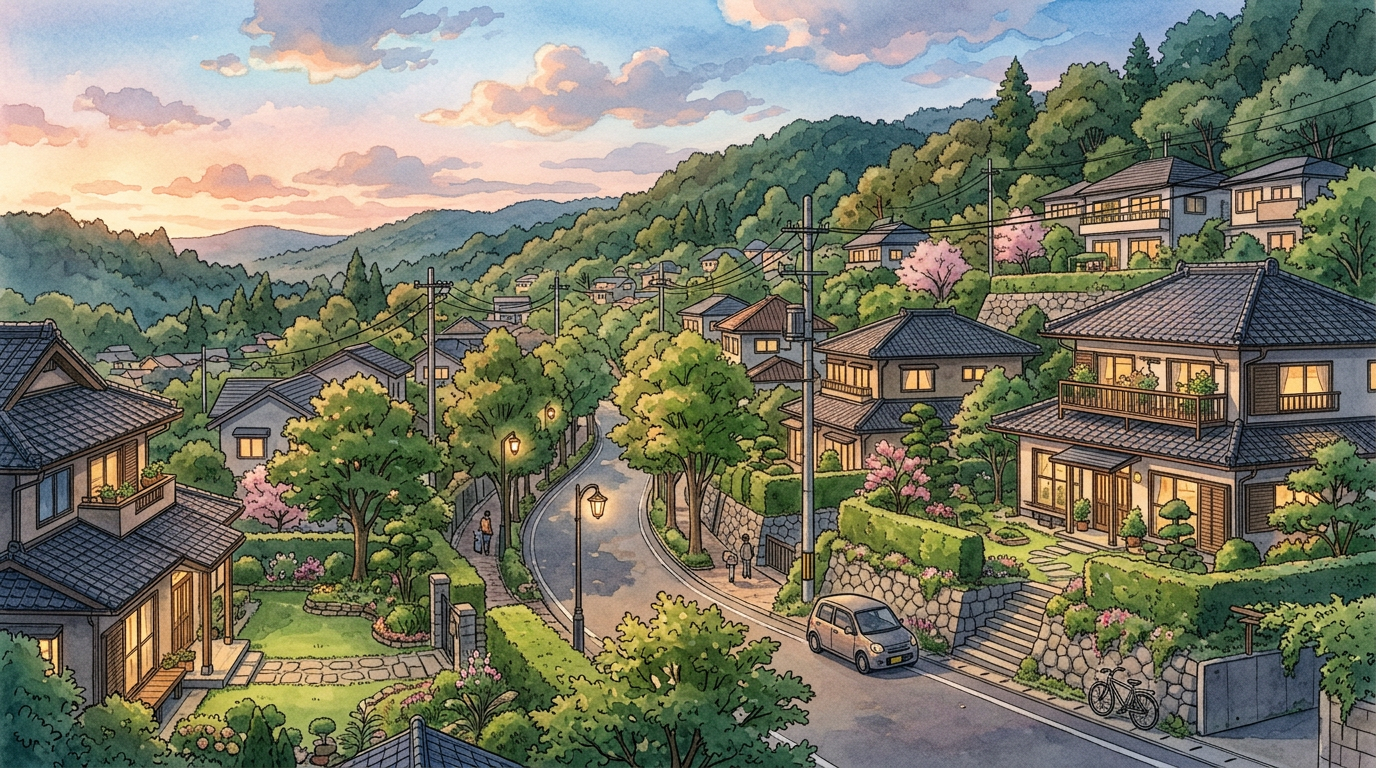

Location Advantages & Connectivity in District 19

Recreation Lane's positioning within District 19 provides strategic advantages that significantly enhance lifestyle quality and property value. The location balances urban convenience with suburban tranquility—a rare combination in Singapore.

Public Transport Connectivity

MRT Access: The development enjoys excellent MRT connectivity with two major stations within convenient walking distance. Serangoon MRT (North East Line) is approximately 800 meters (10-minute walk) from Recreation Lane, while Hougang MRT is roughly 1,000 meters (12-minute walk) away. Both stations provide direct connections to the CBD, making commuting to business districts straightforward and efficient.[1][2]

Bus Services: Multiple bus routes operate along Upper Serangoon Road and nearby corridors, including services 82 and 113, providing additional connectivity options. Bus connections reach the CBD in approximately 20 minutes via the PIE (Pan Island Expressway), offering flexibility for commuters preferring public transport.

Expressway Access: Proximity to the CTE (Central Expressway) and PIE provides rapid vehicular access to all parts of Singapore. Drivers can reach Changi Airport in approximately 30 minutes, the Marina Bay area in 20 minutes, and the western regions in 25-35 minutes.

Education Facilities

District 19's mature estate status means excellent educational options within close proximity. Families benefit from:

- Primary Schools: 5+ primary schools within 2km radius, including established institutions with strong academic records

- Secondary Schools: Multiple secondary schools serving the area, with several ranked among Singapore's top institutions

- International Schools: Several international schools within 15-20 minutes drive, catering to expatriate families

- Preschools & Childcare: Numerous childcare centers and preschools throughout Serangoon and Hougang

This educational infrastructure makes the area particularly attractive for families with children, supporting strong owner-occupier demand and rental appeal to expatriate families.

Shopping & Dining Amenities

Shopping Centers: NEX (Nex Shopping Centre) and Hougang Mall are within 10-15 minutes by car or bus, offering comprehensive retail, dining, and entertainment options. These malls feature major supermarkets, fashion retailers, electronics stores, and entertainment venues.

Hawker Centers & Food Courts: Hougang's renowned hawker centers provide authentic local dining experiences with excellent food at affordable prices. These centers are integral to the neighborhood's character and provide convenient daily dining options for residents.

Dining Diversity: The area offers a mix of local hawker fare, casual restaurants, and modern cafes, reflecting Singapore's multicultural food culture. From traditional Chinese, Malay, and Indian cuisines to contemporary fusion restaurants, dining options cater to diverse preferences.

Parks & Recreation

Recreation Lane's name reflects the area's green spaces and recreational facilities. Nearby parks and green corridors provide:

- Walking and jogging paths through landscaped gardens

- Open spaces for outdoor activities and community events

- Proximity to Serangoon Gardens, one of Singapore's most prestigious residential areas with established greenery

- Access to nature reserves and nature trails for weekend exploration

These recreational amenities contribute significantly to quality of life and property appeal, particularly for families and health-conscious individuals.

Healthcare Facilities

District 19 has good coverage of healthcare facilities including polyclinics, private medical clinics, and proximity to major hospitals. Residents have convenient access to medical services for routine healthcare and emergencies.

Financing Guide for Buyers: Mortgages, Down Payments & CPF

Understanding financing options is crucial for making purchasing decisions. Most buyers require mortgage financing, and several options exist for Singapore property purchases. Homejourney provides tools to help you assess affordability and explore financing scenarios.

Down Payment Requirements

For private property purchases in Singapore, the standard down payment is 20% of the purchase price, paid to the seller at the point of sale. This down payment requirement means:

- For a S$1,000,000 property: S$200,000 down payment required

- For a S$750,000 property: S$150,000 down payment required

- For a S$500,000 property: S$100,000 down payment required

Some developers offer deferred payment schemes or reduced down payments during launch periods, but these are exceptions. Standard market practice requires the full 20% at point of sale.

Mortgage Financing Options

Bank Mortgages: Singapore's major banks (DBS, OCBC, UOB, Maybank, CIMB) offer residential mortgages with typical terms of 25-30 years. Current mortgage rates (February 2026) range from 4.0% to 4.5% depending on the bank and your credit profile. Most banks offer fixed-rate and floating-rate options.

Loan-to-Value (LTV) Limits: Banks typically lend up to 75-80% of the property value for owner-occupiers and 60-70% for investors. This means:

- Owner-occupier buying S$1,000,000 property: Can borrow S$750,000-800,000, requiring S$200,000-250,000 cash

- Investor buying same property: Can borrow S$600,000-700,000, requiring S$300,000-400,000 cash

Mortgage Duration: Most mortgages are structured for 25-30 years, with monthly payments calculated based on the interest rate and loan tenure. Longer tenures reduce monthly payments but increase total interest paid.

CPF Usage for Property Purchase

Singapore citizens and permanent residents can use CPF (Central Provident Fund) savings for property purchases, subject to conditions:

- Down Payment: CPF can be used for the 20% down payment

- Mortgage Repayment: CPF can be used to service monthly mortgage payments (up to a maximum monthly amount)

- Stamp Duties: CPF can cover legal fees and stamp duties associated with purchase

- Minimum CPF Balance: A minimum CPF balance must be maintained (currently S$160,000 for retirement purposes)

Using CPF for property purchases is common in Singapore and can significantly reduce the cash required at purchase. Consult with your bank and CPF board regarding your specific eligibility and options.

Additional Buyer Stamp Duty (ABSD)

Singapore imposes Additional Buyer's Stamp Duty (ABSD) on property purchases, with rates varying based on buyer profile:

| Buyer Profile | ABSD Rate |

|---|---|

| Singapore Citizens (1st property) | 0% |

| Singapore Citizens (2nd property) | 5% |

| Singapore Citizens (3rd+ property) | 10% |

| Permanent Residents | 5% |

| Foreign Buyers | 20% |

ABSD is calculated on the purchase price and must be paid within 14 days of purchase. This is a significant cost factor that must be included in your total purchase budget.

Estimated Monthly Payment Examples

To illustrate affordability, here are estimated monthly mortgage payments for different unit types at Non-landed Housing Development (assuming 25-year mortgage at 4.2% interest rate, with 20% down payment and CPF usage for down payment):

- 1-Bedroom (S$650,000): Approximately S$2,150/month (after CPF down payment)

- 2-Bedroom (S$1,050,000): Approximately S$3,480/month (after CPF down payment)

- 3-Bedroom (S$1,400,000): Approximately S$4,640/month (after CPF down payment)

Disclaimer: These are estimates based on February 2026 interest rates and assumptions. Actual payments vary based on bank, interest rate, loan tenure, and individual CPF usage. Use Homejourney's mortgage calculator for personalized estimates.

Check your buying power and explore financing options with our mortgage calculator.

Step-by-Step Buying Process: From Search to Ownership

Understanding the property buying process helps you navigate the transaction smoothly and avoid common pitfalls. Singapore's property purchase process is highly regulated and transparent.

Step 1: Property Search & Selection

Begin by browsing available units at Non-landed Housing Development on Homejourney. Filter by unit type, price range, and preferred floor level. Review unit details, floor plans, and high-resolution photography. Create a shortlist of units that meet your requirements and budget.

Homejourney provides comprehensive property information including unit specifications, pricing history, and market analysis to support your decision-making.

Step 2: Arrange Property Viewing

Schedule viewings for your shortlisted units. During viewings, assess the unit condition, layout practicality, natural light, views, and overall appeal. Visit at different times of day to understand traffic patterns and neighborhood activity. For new launches, visit the show units to understand the quality and finishes.

Contact a Homejourney agent to arrange viewings and receive professional guidance throughout the process.

Step 3: Financial Preparation & Pre-Approval

Before making an offer, secure mortgage pre-approval from your preferred bank. Provide financial documents including payslips, tax returns, CPF statements, and bank statements. The bank will assess your borrowing capacity and provide a pre-approval letter indicating the maximum loan amount.

Simultaneously, ensure you have sufficient funds for the down payment, ABSD, and legal fees. Consult with a financial advisor to optimize CPF usage and overall financing strategy.

Step 4: Make an Offer & Negotiate

Once you've identified your preferred unit, your agent will present an offer to the seller. In Singapore's property market, offers are typically made at or near the asking price for competitive properties. Negotiations may occur, particularly for older properties or during slower market periods.

Your offer should be contingent on mortgage approval and satisfactory legal review. Once the seller accepts your offer, you'll proceed to the next stage.

Step 5: Legal Review & Contract Signing

Engage a property lawyer to review the sale and purchase agreement. The lawyer will:

- Review all contract terms and conditions

- Conduct title searches to verify ownership and identify any encumbrances

- Advise on legal implications and potential issues

- Negotiate any necessary amendments to standard terms

Once satisfied, you'll sign the sale and purchase agreement. This legally binding contract outlines the purchase price, completion date, and all terms and conditions.