Meyer Blue for sale listings are attracting strong interest from Singapore buyers who want a rare freehold East Coast address, unblocked sea or city views, and MRT connectivity in prestigious District 15.

As a Homejourney researcher who has lived in the East Coast and walked Meyer Road dozens of times, this guide pulls together everything a serious buyer or investor needs to know before committing to a unit at Meyer Blue – prices, layouts, location, schools, financing and investment potential – in one trustworthy, data-backed resource.

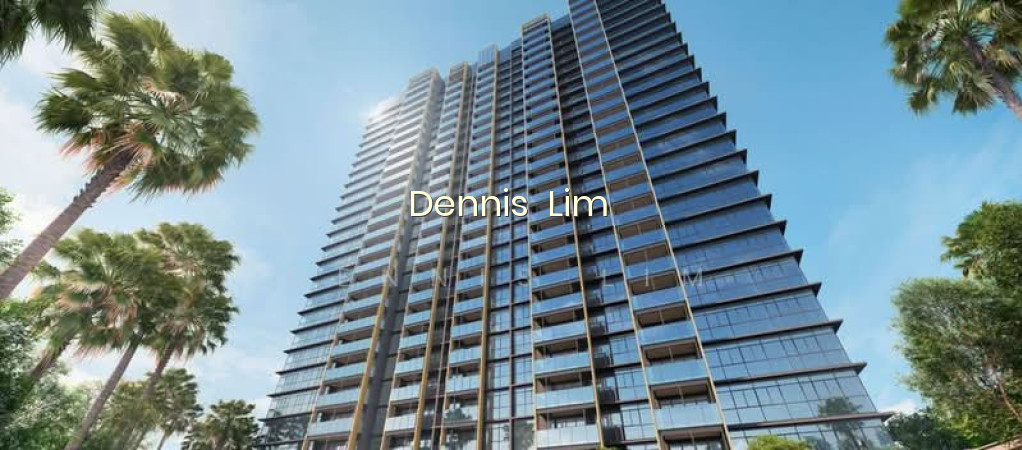

Meyer Blue Overview: Development Snapshot

Meyer Blue is a new freehold luxury condominium at Meyer Road in District 15 (Marine Parade / East Coast), sitting on the former Meyer Park site and jointly developed by UOL Group and Singapore Land (SingLand).[1][2][4]

The project is positioned as an exclusive, low-density development with about 226–250 units on a 96,672 sq ft freehold land parcel, offering unblocked city and sea views from many stacks.[1][2][3][4]

Key Facts at a Glance

| Attribute | Details (indicative, 2026) |

|---|---|

| Developer | UOL Group & Singapore Land (SingLand)[2][4] |

| Address | Along Meyer Road, District 15 (Marine Parade / East Coast)[1][2][5] |

| Tenure | Freehold[2][4] |

| Site Area | Approx. 96,672 sq ft[3][4] |

| No. of Units | Approx. 226–250 luxury apartments[2][3][4] |

| Former Site | Former Meyer Park, sold en bloc for about $392.18M[2][6] |

| Land Cost | About $1,668 psf ppr (land)[2][6] |

| Planning Area | Marine Parade, District 15[5] |

| Nearest TEL MRT | Katong Park (TE24) & Tanjong Katong / Amber (TEL), walking distance[1][2][5][7] |

UOL and SingLand have a strong track record of premium condos such as Meyer House and Avenue South Residence, which gives buyers confidence in build quality, design and long‑term management – especially important for freehold assets you may hold for decades.

In the East Coast, Meyer Road is often called the “Nassim of the East” for its combination of landed homes, sea views and low-density luxury condos.[1] Living here feels very different from more crowded parts of Marine Parade: on evening walks, you mostly see residents and joggers rather than heavy through-traffic.

Available Units for Sale at Meyer Blue

Because Meyer Blue is a relatively exclusive, single-tower freehold project, available units at any point in time can be limited. Serious buyers should monitor live inventory and act quickly when preferred stacks or facing become available.

Typical Unit Mix at Meyer Blue (Indicative)

The final unit mix is subject to the developer’s official release, but based on land size, positioning in the Meyer cluster and comparable new launches, you can expect a luxury-focused mix catering to own-stay families and affluent investors:

- 2‑Bedroom and 2‑Bedroom + Study

- 3‑Bedroom and 3‑Bedroom Premium

- 4‑Bedroom Premium and/or 4‑Bedroom with private lift

- Large 4‑ to 5‑Bedroom or penthouse units (limited)

Studios and compact 1‑bedroom units are less common along Meyer Road freehold projects, as the area traditionally targets family and long-term owner-occupiers rather than purely investor shoebox demand.

Current Price Range & PSF Expectations (2026)

Given the land cost of about $1,668 psf ppr and strong demand for freehold D15 condos, early market expectations for Meyer Blue’s launch pricing have generally been in the broad region of the mid‑$2,6xx to low‑$3,0xx psf range, depending on floor level, facing and unit size.[2][6][7]

As of 2026, buyers considering Meyer Blue typically budget around:

- 2‑Bedroom: Roughly from low $2.XM to around $3M+, depending on level and layout (estimate)

- 3‑Bedroom: Around high $2.XM to mid‑$3M+ (estimate)

- 4‑Bedroom & larger: From about high $3M+ to $5M+ for premium or penthouse-type layouts (estimate)

Important disclaimer: These are indicative expectations based on land cost, URA caveats for comparable D15 launches, and 2025–2026 freehold pricing trends. Actual developer prices and resale prices can differ. Always verify real-time prices and availability on Homejourney’s live listings and URA’s latest caveats.

Most Popular Buyer Profiles & Unit Types

- Young professional couples & DINKs: 2‑Bedroom and 2‑Bedroom + Study, often choosing high floors facing the sea or city for a long-term own‑stay.

- Upgrader families from Marine Parade, Katong, Bedok, or the East: 3‑ and 4‑Bedroom units, drawn by the proximity to good schools and East Coast Park.

- Legacy planners: Larger 4‑Bedroom or penthouse units purchased under family trusts or as multi‑generation homes, leveraging freehold tenure.

- Investors: Efficient 2‑Bedroom layouts that appeal to senior executives working in CBD/Marina Bay and expats who want to be near the coast.

Next step: View all units for sale at Meyer Blue in real time via Homejourney’s verified listings: Property Search . Use the query "Meyer Blue" and set status to "For Sale" to see current available units.

Why Buyers Choose Meyer Blue

From years of walking the stretch between Meyer Road and East Coast Park, what stands out most is how peaceful the neighbourhood remains despite being minutes from the city. Meyer Blue builds on this with a modern, resort-like development that is intentionally low-density and lifestyle-focused.[1][2][4]

Key Selling Points at a Glance

| Key Benefit | Why It Matters to Buyers |

|---|---|

| Freehold in Prime D15 | Land-scarce freehold stock near the coast and CBD offers long-term value and legacy planning. |

| Prestigious Meyer Road address | Regarded as the top tier of East Coast living, with a mix of landed and luxury condos.[1] |

| Unblocked sea and city views | High-floor units can enjoy panoramic views that are hard to replicate inland.[1][3] |

| Thomson–East Coast Line MRT | Short walk to Katong Park (TE24) and future TEL stations for direct CBD access.[1][2][5][7] |

| Near East Coast Park | Weekend cycling, beach walks and hawker food at East Coast Lagoon are minutes away. |

| Strong developer reputation | UOL & SingLand track record gives confidence on build quality, finishings and management.[2][4] |

| Low-density, private enclave | Quieter, more exclusive feel versus the busier Marine Parade central stretch.[1][3] |

Lifestyle Benefits Only Locals Talk About

Living off Meyer Road, you can realistically walk or cycle to East Coast Park in under 10 minutes via the underpass at Meyer Road, depending on which block and which traffic crossing you use. Many residents do evening walks from Meyer Road to the park, grab satay or seafood at East Coast Lagoon, then head back via the park connector.

Weekend routines often involve:

- Morning coffee at the Katong or Joo Chiat café belt (around 5–10 minutes’ drive).

- Quick grocery runs to Parkway Parade or Katong V.

- Nighttime drives to the CBD or Marina Bay in about 10–15 minutes when ECP traffic is light.

This combination of coastal living, food culture and CBD accessibility is why East Coast – especially Meyer – consistently commands a loyal local buyer base.

Price Analysis & PSF Guide (2026)

Because Meyer Blue is a freehold new launch in one of the most prestigious D15 micro-locations, it sits at the upper end of the East Coast price spectrum. Understanding how its expected pricing compares with nearby projects is crucial for making a confident purchase decision.

Land Cost & Implied Launch Pricing

The former Meyer Park site was sold for about $392.18 million, translating to roughly $1,668 psf per plot ratio.[2][6] Factoring in construction, financing, marketing and developer margins, analysts typically expect launch prices meaningfully above land cost, especially for freehold luxury projects.

For context, other D15 launches (Tembusu Grand, Grand Dunman, The Continuum) have land bids around $1,060–1,204 psf ppr for 99‑year or mixed tenure land, with launch prices often in the low‑ to mid‑$2,0xx psf range depending on project and phase.[7] Meyer Blue’s higher land cost and freehold status naturally push it into a higher PSF band.

Meyer Blue vs Other District 15 Projects (High-Level)

Based on public project comparisons for the D15 collection:[7]

- Many D15 launches like Tembusu Grand and Grand Dunman are 99‑year leasehold with larger unit counts (600–1000+ units).[7]

- The Continuum and Meyer Blue stand out as freehold projects in D15; Meyer Blue is positioned as an exclusive, seaview-centric development along Meyer Road.[7]

- Meyer Blue’s land bid of about $1,668 psf ppr is notably higher than some other D15 sites (around $985–1,204 psf ppr), reflecting its prime Meyer Road frontage and sea proximity.[7]

Value Assessment for Buyers

When comparing Meyer Blue with other Singapore condos for sale in D15, consider:

- Tenure: Freehold vs 99‑year – freehold provides longer holding horizon and stronger legacy value, especially near the coast.

- Micro-location: Meyer Road’s status as a top-tier address vs inner D15 (Joo Chiat, Telok Kurau) or further inland projects.

- Density & facilities: Low-density, single-block resort feel vs mega-developments with more units but potentially more crowding.

- View premiums: Sea and city views command a lasting premium that can support resale values.

For data-driven buyers, Homejourney’s Meyer Blue project page consolidates URA transaction data and price trends so you can benchmark $PSF against other D15 properties easily: Projects Directory and the dedicated Meyer Blue project profile Projects .

Location & District 15 Lifestyle Advantages

Meyer Blue’s location is one of its biggest selling points. It sits in Marine Parade’s Meyer enclave, within District 15 – an area that consistently draws both local families and expats for its blend of coastal living, schools and amenities.[1][2][5]

MRT & Road Connectivity

- Thomson–East Coast Line (TEL): Meyer Blue is within walking distance to the upcoming Katong Park (TE24) and other TEL stations such as Amber or Tanjong Katong, giving direct or convenient connections to Marina Bay, Shenton Way and Orchard.[1][2][5][7]

- Driving via ECP: A short drive via the East Coast Parkway gets you to the CBD, Marina Bay, Suntec, Changi Airport and other key nodes. In off-peak hours, CBD runs from Meyer Road can be around 10–15 minutes.

- Bus connectivity: Multiple bus services run along Mountbatten Road and Marine Parade Road, connecting to Paya Lebar, Eunos, Orchard and other parts of the island.

From first-hand experience, the practical benefit here is consistently predictable commuting. Even when ECP is busy, you usually have alternate routes via Nicoll Highway, Kallang–Paya Lebar Expressway (KPE) or Mountbatten Road depending on your destination.

Schools Near Meyer Blue

District 15 is known for a wide range of primary, secondary and international schools. According to publicly available information and URA/OneMap school distance tools (always verify exact distances and 1km/2km bands before decision):

- Primary schools (within a short drive; check specific distance bands): Kong Hwa School, Tanjong Katong Primary, Haig Girls’ School.[1]

- Secondary & integrated programmes: Dunman High School, Chung Cheng High School (Main), Tanjong Katong Girls’ School, Tanjong Katong Secondary.[1]

- International options: Canadian International School (Tanjong Katong campus), EtonHouse International, Chatsworth (for nearby campuses), among others.

Parents in the East often choose Meyer and Amber areas as a balance between school options and lifestyle; you’re not directly next to a school (less congestion) but still within a short commute for morning drop-offs.

Shopping, Amenities & Food

From Meyer Blue, you are a short drive from several established malls and lifestyle nodes:[1]

- Parkway Parade: The main heartland mall for East Coast, with supermarkets, clinics, banks, enrichment centres and F&B.

- I12 Katong: Refreshed mall with cinema, restaurants and boutique shops.

- Katong/Joo Chiat shophouses: Known for Peranakan culture, cafés, dessert bars and late-night eateries.

- Neighbourhood grocers & cafés: Smaller grocers and bakeries scattered through Mountbatten and Marine Parade.

Insider tip: For late dinners, many East Coast residents swing between Katong’s Tanjong Katong Road eateries, Old Airport Road Food Centre, and the East Coast Lagoon Food Village – all within 5–10 minutes’ drive from Meyer Blue.

Parks, Recreation & Beachfront Living

Meyer Blue is very close to East Coast Park, one of Singapore’s largest and most beloved recreational spaces, accessible via the Meyer Road underpass and park connectors. URA and NParks have progressively upgraded this coastal stretch with better cycling paths, landscaping and F&B nodes.

Typical weekend activities residents enjoy:

- Leisure cycling or jogging along the continuous East Coast Park connector.

- Beach picnics and barbecues at park chalets or open pits (advance booking via NParks required).

- Watersports such as stand‑up paddling or kayaking via the sea sport providers.

This access makes Meyer Blue attractive not just as a place to sleep, but as a lifestyle hub – an important consideration if you are choosing your long-term home rather than a purely investment property.

Layouts, Liveability & Buyer Profiles

While final floorplans are determined by the developer, Meyer Blue is expected to follow the East Coast luxury template: efficient yet generous layouts with a focus on liveability and views rather than ultra-compact “investment shoebox” units.

What to Look For in Meyer Blue Layouts

- Orientation: North‑South oriented stacks tend to enjoy better cross-ventilation and avoid direct afternoon west sun; some stacks are also designed to capture sea or city views based on project information.[1][3][7]

- Balcony size vs internal space: With seaview projects, balconies can be a major lifestyle feature, but consider indoor usable area if you work from home.

- Bedrooms & flexibility: 3‑Bedroom + utility layouts are popular with families who need a helper’s room or extra storage.

- Private lift vs common lift lobby: Higher-end 4‑Bedroom or penthouse units may come with private lifts – a prestige and privacy factor.

For a deeper framework on evaluating unit types and sizes, you can refer to Homejourney’s detailed approach in similar guides such as: Urban Residences Unit Types & Size Guide for Buyers | Homejourney and Visioncrest Unit Types & Size Guide for Buyers | Homejourney . The same analytical lens applies to Meyer Blue’s floorplans.

Financing Guide for Meyer Blue Buyers

Buying a freehold D15 property is a major commitment. Homejourney emphasises affordability checks, transparent loan comparisons and safe decision-making before you pay any booking fee or exercise an Option to Purchase (OTP).

Rough Monthly Payment Estimates

To illustrate affordability, here is a simplified example assuming a 75% bank loan (standard MAS LTV for buyers with no outstanding housing loan), 30‑year tenure and an indicative interest rate of around 3.0–3.5% p.a. (rates vary daily; always check live rates).

| Unit Price (Example) | Loan (75%) | Approx. Monthly Payment* |

|---|---|---|

| $2.4M (2‑BR example) | $1.8M | ≈ $7,600–$8,100 per month |

| $3.4M (3‑BR example) | $2.55M | ≈ $10,800–$11,500 per month |

| $4.5M (4‑BR example) | $3.375M | ≈ $14,300–$15,300 per month |

*These are broad estimates only and will vary with interest rates, loan tenure, age, income, TDSR calculations and bank policies. Always run your own calculations and consult a licensed banker or financial advisor.

Down Payment, CPF & Cash Requirements

Under current MAS and CPF housing rules (subject to change):

- Minimum down payment: Typically 25% for buyers taking a bank loan; at least 5% must be in cash, with the remaining 20% in cash and/or CPF Ordinary Account (OA), subject to CPF limits.

- Buyer’s Stamp Duty (BSD): Payable on the purchase price or market value, whichever is higher, using IRAS’s prevailing BSD rates.

- CPF usage: CPF OA can be used for down payment and monthly instalments, subject to Valuation Limit and Withdrawal Limit rules.

Because Meyer Blue units are high-value, many buyers use a combination of CPF OA and cash for the 25% down payment and stamp duties, while keeping enough liquidity for renovation, furniture and emergency reserves.

ABSD Considerations (Important)

Additional Buyer’s Stamp Duty (ABSD) applies depending on your residency status and number of existing properties owned in Singapore, as per current IRAS rules. In general:

- Singapore Citizens buying their first residential property pay no ABSD, only BSD.

- Second and subsequent properties attract higher ABSD rates, which can significantly impact the total cash/CPF outlay.

- PRs and foreigners have different ABSD structures which can be substantial.

Because ABSD policy has changed multiple times in recent years, always confirm the latest rates from IRAS or a qualified lawyer before committing to any purchase.

Next step: Use Homejourney’s mortgage and bank rate tools to check your buying power safely before you book a unit at Meyer Blue: Bank Rates . For more in-depth financing strategies, see similar frameworks in Urban Residences Home Loan & Financing Guide | Homejourney and Visioncrest Home Loan & Financing Guide for Buyers | Homejourney .

Step-by-Step Buying Process at Meyer Blue

Homejourney encourages buyers to follow a structured, safety-first process when purchasing a new launch or resale unit at Meyer Blue.

1. Pre‑Assessment & Budget Planning

- Check your loan eligibility and indicative maximum purchase price using Mortgage Rates and bank calculators.

- Work out how much CPF OA and cash you can allocate, keeping an emergency buffer.

- Factor in BSD, potential ABSD, legal fees, renovation and furnishing.

2. Shortlist Units & Stack Selection

- Browse verified Meyer Blue for sale listings on Homejourney: Property Search (search “Meyer Blue”).

- Compare unit types, floors and facing based on your priorities: view, privacy, layout, price.

- Check URA Master Plan for future developments nearby to understand potential view obstructions or enhancements.

3. Viewing & Due Diligence

- Arrange a showflat viewing or unit viewing via a trusted agent: or .

- Clarify all fees, maintenance charges and facility details with the salesperson.

- For resale units (in future), verify recent URA caveats and past transaction history via Projects Directory .

4. Booking & Option to Purchase (OTP)

- For new launch: Once you select a unit, you typically pay a booking fee (usually 5% of purchase price) to secure an OTP.

- For resale: Negotiate price and terms, then have your lawyer or agent prepare the OTP.

- Always ensure all details – unit number, price, completion timeline – are correct before signing.

5. Exercise OTP & Loan Finalisation

- Within the OTP validity period (often 2–3 weeks for resale; new launch timelines may differ), instruct your lawyer to exercise the OTP.

- Finalise your bank loan approval and sign the Letter of Offer.

- Pay the remaining portion of the 20% down payment and applicable stamp duties (BSD/ABSD) within IRAS timelines.

6. Progressive Payments & Handover

- For new launch, payments are made progressively based on construction stages per the standard schedule of payment under the Sale & Purchase Agreement.

- On Temporary Occupation Permit (TOP), you can collect keys, inspect the unit and begin renovation.

- For resale, the completion usually occurs within 8–12 weeks after exercise, subject to agreed terms.

For renovation and move-in, Homejourney also curates trusted service providers – for example, for essential air-conditioning inspection and servicing before you move in: Aircon Services .

Investment Potential: Yield, Demand & Future Upside

As an investor or own-stay buyer with an investment mindset, you should assess both potential rental yield and capital appreciation prospects of Meyer Blue within the context of D15 trends.

Rental Demand Drivers

District 15 is traditionally popular with expats and senior executives who want to stay near the coast but within a short commute of the CBD and Marina Bay.[5] Key demand drivers include:

- Proximity to CBD, Marina Bay, Paya Lebar business hub and Changi Airport.

- Appeal of East Coast lifestyle – parks, beaches, food and international schools.

- Availability of mid- to high-end condos suitable for corporate leases.

Meyer Blue, being freehold and positioned as a luxury project with sea or city views, is well-placed to capture the upper tier of D15 rental demand once completed.

Indicative Rental Yield Framework

Actual rental yields will depend on final acquisition price, market conditions at TOP and tenant profile. As a simple framework:

- If a 2‑Bedroom unit is purchased at, say, $2.4M and rented at $6,500/month, gross yield ≈ 3.25% p.a.

- If a 3‑Bedroom is purchased at $3.4M and rented at $9,000/month, gross yield ≈ 3.18% p.a.

These figures are illustrative only and depend on 2026–2030 rental market conditions, interest rates and expat demand. For a systematic approach to yield analysis, see Homejourney’s methodologies in Urban Residences Investment Returns: Rental Yield Analysis | Homejourney and Visioncrest Investment Returns: Rental Yield Analysis 2026 .

Capital Appreciation Outlook

Several structural factors support Meyer Blue’s long-term price resilience:

- Limited freehold coastal land: New freehold supply along Meyer Road is scarce, while older stock may be ripe for future rejuvenation.

- Upcoming TEL & infrastructure: The full opening of the Thomson–East Coast Line enhances East Coast accessibility, typically supportive for pricing near stations.[1][2][5]

- Changing lifestyle preferences: Post-pandemic, buyers place greater emphasis on space, greenery and outdoor access – all strong suits for Meyer Blue.

To refine your capital appreciation thesis, you can reference transaction data and price trend analysis on Projects Directory , as well as broader market coverage from sources such as Straits Times Housing News or Business Times Property for macro trends impacting prime condos.

How Homejourney Protects Buyers at Meyer Blue

Homejourney is built around user safety, verification and transparent information – especially important for big-ticket decisions like buying at Meyer Blue.

Verified Listings & Data Transparency

- Listings for Meyer Blue for sale on Homejourney go through checks to reduce fake or outdated postings.

- Key information such as unit size, asking price and floor level is clearly presented so you can compare fairly.

- Where possible, URA transaction data and price histories are surfaced on Projects to help you cross-check developer or resale pricing.

Customer-Centric Support & Feedback

- Homejourney continuously incorporates buyer feedback to improve search filters, financing tools and service provider recommendations.

- Agents and partners who work with Homejourney are encouraged to prioritise clear disclosure of fees, timelines and obligations.