Bukit Loyang Estate stands as one of Singapore's most coveted freehold landed developments, offering discerning buyers the rare combination of spacious semi-detached homes, prime District 17 location, and strong capital appreciation potential. Whether you're a first-time buyer, upgrader, or savvy investor, this comprehensive guide walks you through everything you need to know about purchasing property at Bukit Loyang Estate.

At Homejourney, we prioritize your safety and confidence in every property decision. We've compiled verified transaction data, current market pricing, and actionable insights to help you make informed choices about buying at this prestigious development.

Table of Contents

- Property Overview & Market Position

- Available Units For Sale

- Why Buy at Bukit Loyang Estate

- Price Analysis & Market Trends

- Location Advantages in District 17

- Home Loan & Financing Guide

- Step-by-Step Buying Process

- Investment Potential & Rental Yield

- Frequently Asked Questions

Property Overview & Market Position

What Makes Bukit Loyang Estate Special

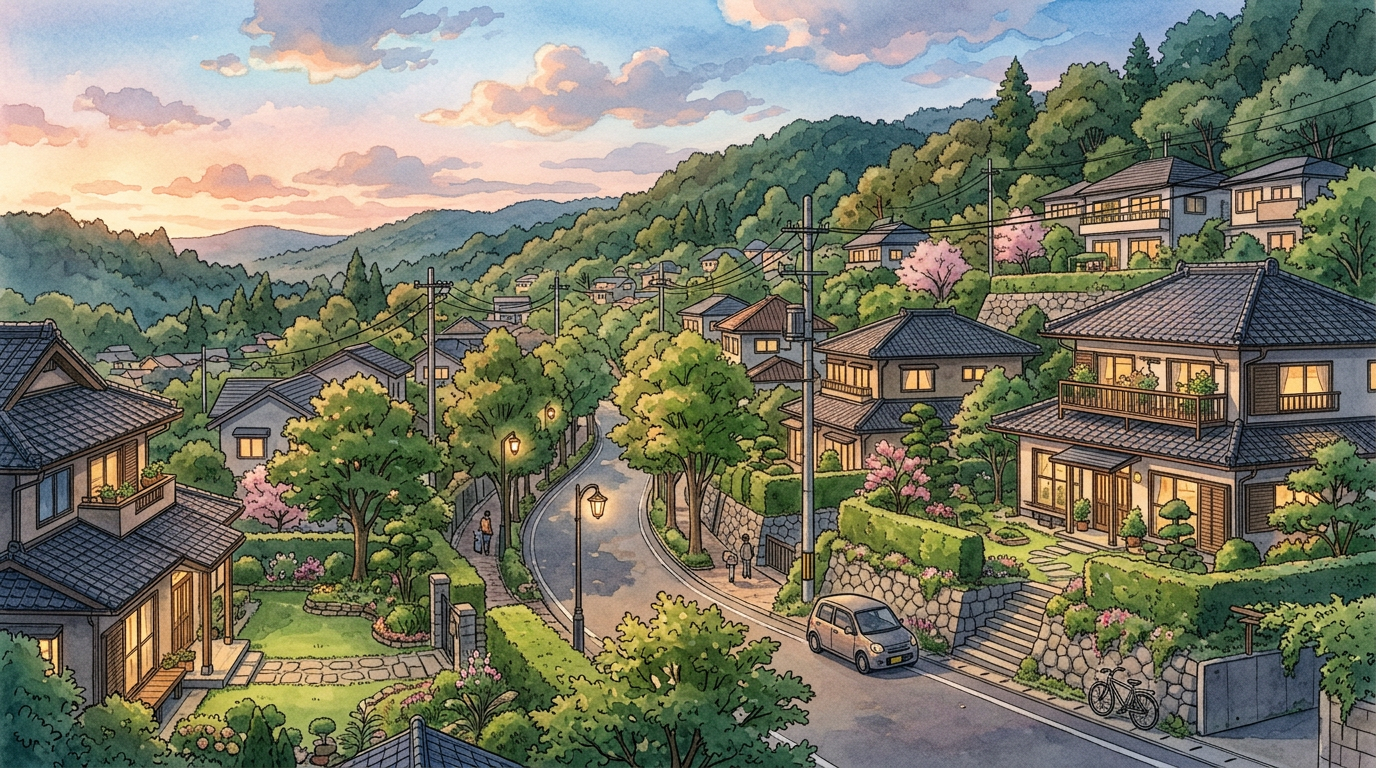

Bukit Loyang Estate represents a unique opportunity in Singapore's property market. Located in the heart of District 17 (Changi-Loyang), this exclusive freehold development features semi-detached homes that command premium pricing due to their spacious layouts, land area, and strategic location. Unlike condominiums, these landed properties offer complete ownership of both building and land—a significant advantage for long-term wealth building.

The estate has consistently demonstrated strong market performance, with recent transactions showing prices ranging from $3.5 million to $5.8 million depending on unit size and specifications. The development's appeal lies in its blend of suburban tranquility with urban convenience, attracting families, professionals, and investors seeking quality living space.

Development Characteristics

Bukit Loyang Estate comprises semi-detached units situated on Jalan Batalong East, Jalan Chelagi, Jalan Kelempong, and Jalan Mariam. All properties carry freehold tenure, meaning you own the land indefinitely—a rare and valuable feature in Singapore's property landscape. The development was completed in 2008, with TOP (Temporary Occupation Permit) issued that same year, ensuring mature infrastructure and established community amenities.

The semi-detached format provides significantly more space than typical condominiums, with units ranging from approximately 3,000 to 6,500 square feet of built-up area. This makes Bukit Loyang Estate particularly attractive for families requiring multiple bedrooms, home offices, or those seeking investment properties with strong rental appeal.

Available Units For Sale at Bukit Loyang Estate

Current Market Availability

Bukit Loyang Estate maintains consistent market activity with semi-detached properties regularly available for purchase. Based on recent transaction data, you can expect to find units in various configurations, though the market moves relatively quickly given the development's prestige and freehold status.

Current asking prices in the market range from approximately $3.5 million to $5.8 million, with price per square foot (PSF) typically between $884 to $1,683 PSF depending on unit size and condition. Larger units with more land area command premium pricing but offer exceptional value for buyers seeking spacious family homes or investment properties.

Typical Unit Specifications

| Unit Type | Built-Up Area | Land Area | Typical Price Range | Price per Sqft |

|---|---|---|---|---|

| Semi-Detached (Standard) | 3,250-3,500 sqft | ~3,300 sqft | $3.9M - $5.5M | $1,200 - $1,683 |

| Semi-Detached (Large) | 6,000-6,500 sqft | ~6,000+ sqft | $5.5M - $5.8M | $884 - $1,000 |

Browse Available Units: To view current listings and units available for sale at Bukit Loyang Estate, visit Property Search where you can filter by price, size, and specific requirements. Homejourney's verified listings ensure you're viewing accurate, current information from trusted sources.

Property Characteristics You'll Find

- Freehold Tenure: All units carry freehold status with no lease expiry concerns

- Semi-Detached Layout: Spacious homes with private land ownership

- Multi-Bedroom Configurations: Typically 4-5 bedrooms with multiple bathrooms

- Modern Amenities: Many units feature updated kitchens, air conditioning, and modern finishes

- Development Potential: Premises suitable for construction up to 3.5 storeys, offering renovation and expansion opportunities

- Mature Infrastructure: Established estate with 18+ years of proven performance

Why Buy at Bukit Loyang Estate

Freehold Ownership Advantage

The most compelling reason to buy at Bukit Loyang Estate is freehold ownership. Unlike leasehold properties that depreciate as lease years decline, freehold properties maintain and appreciate in value indefinitely. This makes Bukit Loyang Estate an exceptional long-term investment, particularly for buyers planning to hold for 20+ years or pass properties to future generations.

Freehold status also eliminates concerns about lease renewal costs, which can be substantial for aging leasehold properties. This financial certainty appeals strongly to families and investors seeking predictable, appreciating assets.

Spacious Living in Prime Location

Bukit Loyang Estate offers what most Singapore properties cannot: substantial living space in a prime location. With built-up areas ranging from 3,250 to 6,500 square feet, these homes provide room for growing families, home offices, and entertaining. The private land ownership means you control your own outdoor space—gardens, parking, and expansion possibilities.

Located in District 17, you're positioned in one of Singapore's most desirable eastern regions, combining suburban peace with proximity to vibrant Changi and Loyang areas. The location offers the best of both worlds: quiet residential living with easy access to shopping, dining, and entertainment.

Strong Investment Fundamentals

Transaction data from recent years demonstrates consistent price appreciation. Properties that sold for approximately $3.1 million in 2021 now command $5.5 million or more, representing significant capital gains. This appreciation reflects strong underlying demand for freehold properties in prime locations, particularly from upgraders and investors.

The rental market remains robust, with monthly rental rates ranging from $5,000 to $11,500 depending on unit size and condition. This translates to gross rental yields of 3-4% annually, attractive for property investors seeking both capital appreciation and income generation.

Established Community & Amenities

As a mature development completed in 2008, Bukit Loyang Estate benefits from established infrastructure and community. Nearby amenities include shopping centers, schools, parks, and dining options. The area has proven its appeal over nearly two decades, with consistent demand and stable property values.

Price Analysis & Market Trends for Bukit Loyang Estate

Current Market Pricing (February 2026)

The current market for Bukit Loyang Estate shows strong pricing momentum. Recent transactions reveal:

- November 2025: 3,268 sqft unit sold for $5.5M ($1,683 PSF)

- October 2025: 3,350 sqft unit sold for $5.5M ($1,642 PSF)

- July 2024: 6,538 sqft unit sold for $5.78M ($884 PSF)

- June 2024: 3,509 sqft unit sold for $4.88M ($1,391 PSF)

These prices demonstrate that standard-sized units (3,250-3,500 sqft) now command $1,600-$1,683 PSF, while larger units offer better PSF value at $884-$1,000 PSF due to economies of scale on land costs.

Historical Price Appreciation

Examining transaction history from 2021 to 2025 reveals impressive appreciation:

| Period | Typical Unit Price | Average PSF | Appreciation |

|---|---|---|---|

| May 2021 | $3.1M | $930 | — |

| 2022-2023 | $3.8M - $4.7M | $1,084 - $1,414 | +23% to +52% |

| 2024-2025 | $4.88M - $5.5M | $1,391 - $1,683 | +57% to +77% |

Over the past four years, standard units have appreciated approximately 77%, translating to roughly 15-17% annualized returns. This exceptional performance reflects strong demand for freehold properties and the scarcity of comparable offerings in Singapore.

Market Outlook & Value Assessment

Several factors support continued appreciation at Bukit Loyang Estate:

- Freehold Scarcity: New freehold developments are extremely rare in Singapore, making existing freehold properties increasingly valuable

- Land Value: The substantial land area (typically 3,300+ sqft) represents significant underlying value independent of building condition

- Development Potential: Properties can be renovated or reconstructed up to 3.5 storeys, offering value-add opportunities

- Prime Location: District 17's continued development and improved connectivity enhance long-term value

- Demographic Demand: Upgraders and families consistently seek spacious homes in established locations

For detailed price trends and transaction analysis, view Projects to access comprehensive market data and historical pricing patterns.

Location Advantages in District 17 (Changi-Loyang)

Strategic District 17 Position

Bukit Loyang Estate's location in District 17 places you in Singapore's thriving eastern corridor. This district encompasses Changi, Loyang, and surrounding areas—regions experiencing significant development and infrastructure improvements. The location balances suburban tranquility with urban convenience, offering residents the best of both environments.

District 17 is characterized by established residential communities, quality schools, and family-friendly amenities. Property values in this district have consistently appreciated, reflecting strong underlying demand from families and investors.

Public Transportation & Connectivity

While Bukit Loyang Estate is primarily a car-dependent area, connectivity has improved significantly:

- Nearest MRT Stations: Tanah Merah Station (Circle Line) is approximately 3-4 km away, providing direct access to central Singapore

- Bus Services: Multiple bus routes serve the estate, connecting to shopping centers, MRT stations, and employment centers

- East Coast Parkway: Direct access to ECP enables quick travel to CBD, airport, and other regions

- Changi Airport: Located approximately 8-10 km away, making the area convenient for frequent travelers

The area's connectivity continues to improve with ongoing infrastructure developments, enhancing accessibility and property values.

Schools & Educational Institutions

Families will appreciate the quality schools within reasonable proximity:

- Primary Schools: Loyang Primary School, Changi Primary School, and other established institutions serve the area

- Secondary Schools: Loyang Secondary School and other quality secondary institutions provide excellent educational options

- International Schools: Several international schools operate in eastern Singapore, serving expat families

- Tertiary Institutions: Polytechnics and universities are accessible via public transport

The concentration of quality schools makes Bukit Loyang Estate particularly attractive for families with children, supporting strong rental demand from expat families seeking family-friendly housing.

Shopping, Dining & Entertainment

The Changi-Loyang area offers diverse shopping and dining options:

- Changi City Point: Major shopping center with retail, dining, and entertainment options

- Changi Business Park: Extensive commercial area with restaurants and services

- Loyang Point: Shopping center serving the eastern region

- Diverse Dining: Hawker centers, restaurants, and cafes offering local and international cuisine

- Entertainment: Cinemas, recreation facilities, and family entertainment venues

These amenities ensure residents enjoy convenient access to shopping, dining, and entertainment without traveling to central Singapore.

Parks, Recreation & Outdoor Activities

The eastern region offers excellent outdoor recreation opportunities:

- East Coast Park: Singapore's longest park offers beaches, cycling paths, water sports, and recreational facilities

- Loyang Wetland Park: Nature reserve providing walking trails and wildlife viewing

- Community Parks: Several neighborhood parks provide green spaces for residents

- Sports Facilities: Tennis courts, swimming pools, and sports centers serve the community

These recreational options make the area ideal for active families and those seeking outdoor lifestyle benefits.

Home Loan & Financing Guide for Bukit Loyang Estate Buyers

Financing Overview for Landed Properties

Financing a Bukit Loyang Estate purchase follows similar principles to other property purchases but with some landed-property-specific considerations. Most banks readily finance freehold landed properties, recognizing their strong collateral value and appreciation potential.

Typical loan-to-value (LTV) ratios for landed properties range from 75-80%, meaning you'll need 20-25% down payment. This is slightly higher than condominium LTV ratios due to the unique characteristics of landed properties.

Down Payment & Initial Costs

For a $5 million purchase at Bukit Loyang Estate, expect these initial costs:

- Down Payment (20-25%): $1.0M - $1.25M

- Stamp Duty on Purchase Agreement: Approximately 1% of purchase price ($50,000)

- Stamp Duty on Mortgage: Approximately 0.4% of loan amount

- Conveyancing Fees: Approximately $1,500-$2,500

- Survey & Legal Fees: Approximately $2,000-$3,000

- Property Inspection & Valuation: Approximately $1,000-$2,000

- Total Initial Costs: Approximately $1.05M - $1.26M (21-25% of purchase price)

These costs vary slightly depending on loan amount, property value, and chosen professional services. Always budget conservatively for these expenses.

Estimated Monthly Mortgage Payments

Using current indicative mortgage rates of 3.5-4.0% over 25-30 year terms:

| Purchase Price | Loan Amount (80%) | Monthly Payment (25yr @ 3.75%) | Monthly Payment (30yr @ 3.75%) |

|---|---|---|---|

| $4.0M | $3.2M | $15,200 | $14,800 |

| $5.0M | $4.0M | $19,000 | $18,500 |

| $5.5M | $4.4M | $20,900 | $20,350 |

Note: These are estimates based on indicative rates. Actual payments depend on your bank's current rates, credit profile, and loan terms. Use Bank Rates to calculate precise payments based on current mortgage rates.

CPF Usage for Landed Property Purchase

If you have CPF savings, you can use your CPF to finance part of the purchase:

- CPF Ordinary Account (OA): Can be used for down payment and loan repayment

- CPF Medisave Account (MA): Cannot be used for property purchases

- CPF Special Account (SA): Cannot be used for property purchases

- Minimum CPF Balance: You must maintain a minimum sum in your CPF account after withdrawal

Many buyers use CPF to reduce their down payment requirement, improving cash flow. Consult your bank and CPF Board for specific eligibility and usage limits.

ABSD (Additional Buyer's Stamp Duty) Considerations

ABSD applies to certain property purchases in Singapore. Key considerations for Bukit Loyang Estate:

- First-Time Buyers: Exempt from ABSD

- Second Property: ABSD of 5% applies if you own another property

- Third+ Property: ABSD of 10% applies

- Foreign Buyers: ABSD of 20% applies (plus 5-10% for additional properties)

- Corporate Buyers: ABSD of 15% applies

ABSD is calculated on the purchase price and must be paid within 14 days of signing the purchase agreement. For a $5 million purchase as a second property, ABSD would be $250,000.

Mortgage Rate Comparison & Bank Selection

Current mortgage rates for landed properties typically range from 3.5% to 4.2% depending on:

- Your credit profile and financial strength

- Loan amount and LTV ratio

- Bank's current promotional rates

- Loan tenure (shorter terms often have lower rates)

Major banks offering competitive rates for landed property financing include DBS, OCBC, UOB, Maybank, and others. Compare rates and terms carefully—a 0.25% difference on a $4 million loan saves approximately $10,000 annually.

Access Bank Rates to compare current mortgage rates from Singapore's major banks and calculate precise monthly payments for your specific purchase scenario.

Step-by-Step Buying Process for Bukit Loyang Estate

Step 1: Property Search & Viewing

Begin by identifying available units that match your requirements:

- Browse current listings on Property Search filtered by Bukit Loyang Estate

- Review property details, photos, and floor plans

- Note asking prices and compare with recent transaction data

- Schedule viewings with agents for properties of interest

- Visit the estate multiple times at different times to assess neighborhood character

During viewings, assess structural condition, layout suitability, and potential renovation needs. Take photos and notes for comparison.

Step 2: Financial Preparation

Before making an offer, ensure your finances are in order:

- Determine your maximum purchase budget based on income and savings

- Obtain mortgage pre-approval from your bank (typically valid for 3-6 months)

- Arrange down payment funds (20-25% of purchase price)

- Calculate total costs including ABSD, stamp duty, and professional fees

- Verify CPF balance and eligibility for CPF withdrawal

Pre-approval demonstrates financial credibility and accelerates the purchase process when you find the right property.

Step 3: Make an Offer & Negotiate

Once you've identified a property:

- Engage a property agent or legal advisor to represent your interests

- Research comparable recent sales to determine fair market value

- Make an initial offer below asking price (typically 5-10% lower)

- Negotiate terms including price, completion timeline, and inclusions

- Agree on conditions such as vacant possession or tenancy arrangements

Most properties involve negotiation. Sellers often expect offers below asking price, and professional representation ensures your interests are protected.

Step 4: Sign Purchase Agreement

Once terms are agreed:

- Your lawyer prepares the Purchase Agreement incorporating agreed terms

- Review the agreement carefully, particularly completion timeline and special conditions

- Sign the agreement and pay stamp duty (approximately 1% of purchase price)

- Pay the initial deposit (typically 5% of purchase price)

- Receive a copy of the signed agreement

The Purchase Agreement is a legally binding contract. Ensure all agreed terms are accurately reflected before signing.

Step 5: Mortgage Application & Approval

After signing the Purchase Agreement:

- Submit formal mortgage application to your chosen bank

- Provide required documentation: purchase agreement, salary certificates, tax returns, CPF statements