Fixed Rate vs Floating Rate Mortgage: Which to Choose & How to Improve Approval Chances

For Singapore home buyers, choose fixed rate mortgages for payment stability if you're risk-averse, or floating rate loans (SORA-based) for potentially lower costs if you can handle fluctuations—while boosting approval by maintaining low debt ratios under TDSR. Homejourney helps you compare live rates from DBS, OCBC, UOB and more to make safe, informed choices in a trusted environment.

This cluster article dives into fixed vs floating rate mortgage which to choose: how to improve approval chances, building on our pillar guide to Singapore home loans. With SORA forecasted at 1-1.39% in 2026, timing your decision is key for HDB upgraders or condo investors.[Pillar: Singapore Home Loan Types Guide]

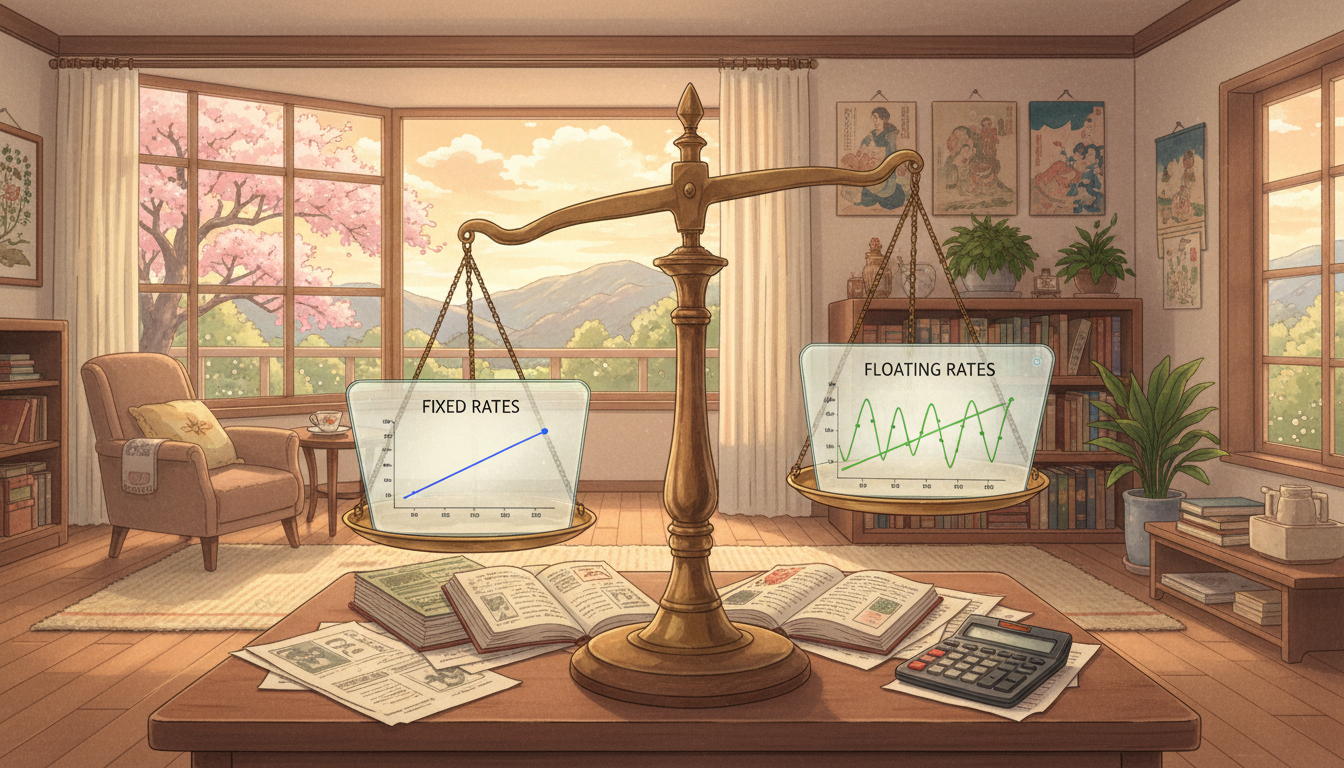

Understanding Fixed Rate vs Floating Rate Mortgages in Singapore

A fixed rate mortgage locks your interest rate for 2-5 years, shielding you from market changes—ideal for families budgeting on a S$500,000 HDB loan where OCBC offers 1.4-1.7% fixed rates, saving predictability amid rising rates post-Q2 2026.[1][3]

Conversely, a floating rate loan ties to SORA (Singapore Overnight Rate Average), the MAS-regulated benchmark published daily by ABS. Most banks add a 0.5-0.8% spread; DBS's SORA +0.5% starts at ~1.2% currently, but could rise to 1.89% by year-end.[1][2]

SORA comes in 3-month (more volatile, lower) or 6-month (smoother, ~0.1-0.2% higher) variants. Track live 3M and 6M SORA on Homejourney's bank rates page for daily updates to time your lock-in.

Current Mortgage Rate Comparison: Fixed vs Floating

As of February 2026, fixed rates range 1.4-1.8% across banks like DBS (1.55% 3Y fixed), OCBC (1.477% 2Y), and UOB (1.35-1.78%). Floating starts lower at 1.11-1.65% (e.g., RHB 1.577% SORA peg).[3][4]

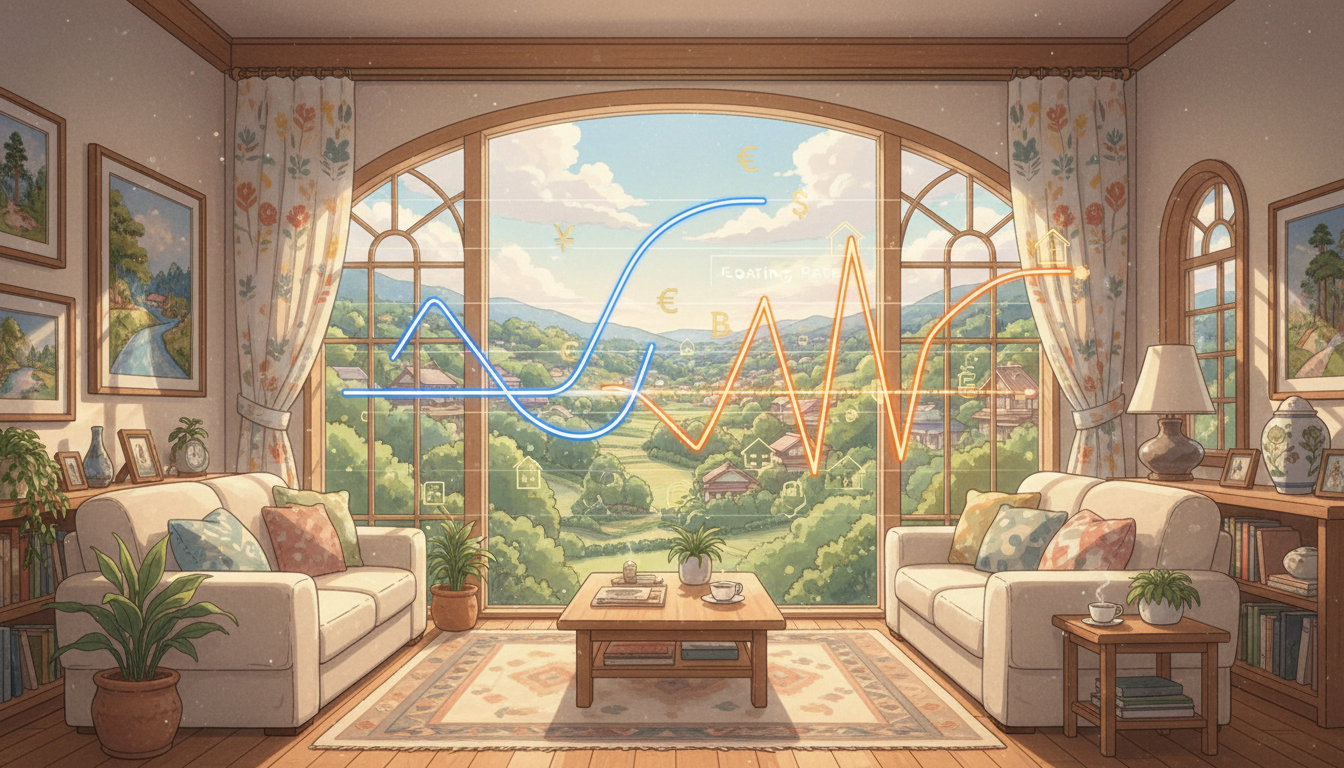

The chart below shows recent interest rate trends in Singapore, highlighting SORA movements and fixed rate stability to guide your mortgage rate comparison:

From the chart, SORA bottomed near 1% in late 2025 before stabilizing—fixed rates offer certainty as forecasts predict a slight uptick to 1.39% by December.[1]

| Type | 2026 Rates | Pros | Cons | Best For |

|---|---|---|---|---|

| Fixed | 1.4-1.8%[1] | Predictable payments | Higher start; penalties | Risk-averse families |

| Floating (SORA) | 1-1.89%[1] | Lower potential | Volatile payments | Investors with buffers |

Pros and Cons: Fixed vs Floating Rate Analysis

- Fixed Rate Pros: Budget certainty—no surprises on your S$3,500 monthly payment for a S$800k condo. DBS offers no early repayment penalties on some packages.[4]

- Fixed Rate Cons: Miss out if SORA falls further; lock-in periods limit flexibility.

- Floating Pros: Benefit from 2026 lows (e.g., Maybank 3M SORA + margin from 1.2%), potentially saving $4,100/year vs fixed on S$500k loan.[1]

- Floating Cons: Payments could jump 20-30% if SORA rises, stressing TDSR compliance.

Choose fixed if planning a family in areas like Punggol (HDB-heavy); floating suits investors flipping in Projects . Homejourney's mortgage calculator simulates scenarios instantly.

Decision Framework: Which Interest Rate Type is Right for You?

Assess your risk tolerance: Conservative? Go fixed. Optimistic on rates? Floating. Factor in loan tenure (25-30 years standard), LTV (up to 75% for HDB), and MSR/TDSR (debt <60% income).

- Check economic outlook: UOB predicts SORA rise post-Q2—lock fixed now.[1]

- Calculate affordability on Homejourney bank rates.

- Match to profile: First-timers favor fixed; refinancers test floating.

How to Improve Home Loan Approval Chances

Boost odds by targeting fixed vs floating rate packages with low spreads. Maintain TDSR under 55%—e.g., S$10k monthly income supports S$5,500 debt max.

- Clean credit: Pay cards on time; banks like HSBC check via Singpass.

- Stable income: 3-6 months' payslips; self-employed use IRAS NOA.

- Low commitments: Minimize car loans before applying.

- Multi-bank submit: Use Homejourney to send one app via Singpass—get offers from DBS, OCBC, UOB, HSBC, Standard Chartered, Maybank, CIMB, RHB instantly.

- Choose flexible packages: Free conversion (FC24) after 2 years for switches.

Homejourney verifies data securely, prioritizing your safety. Apply via our platform for personalized rates—our brokers guide without hard sells. Disclaimer: Rates change; consult professionals. Not financial advice.

FAQ: Fixed vs Floating Rate Mortgages

Q: Fixed rate vs floating rate mortgage which to choose in 2026?

A: Fixed for stability (1.4-1.8%); floating for savings if SORA stays low (~1%). Use Homejourney comparator.[1]

Q: How does SORA affect my floating rate loan?

A: 3M SORA + bank margin (0.5%) sets your rate monthly. Track on Homejourney; expect 1-1.39%.[1][2]

Q: Best bank for fixed rates?

A: OCBC/DBS from 1.4%; compare all on Homejourney—including UOB, HSBC promos.[3][4]

Q: How to improve approval chances?

A: Low TDSR, stable docs, multi-bank apps via Singpass on Homejourney for best odds.

Q: Can I switch from floating to fixed?

A: Yes, via repricing (fees ~0.5-1% of loan); time before lock-in ends. See Fixed vs Floating Rate Mortgages: FAQ Guide | Homejourney .

Ready to choose? Compare fixed vs floating rate options and apply securely on Homejourney bank rates. Search budget-friendly properties at Homejourney search and link back to our pillar for full insights.