The fastest way to choose between a fixed rate and floating rate mortgage in Singapore is to match your interest rate type to your risk tolerance, cash flow stability, and time horizon: fixed rates suit buyers who value certainty and stable monthly instalments, while floating rates suit borrowers who can accept fluctuations in exchange for potential long-term savings in a low or falling rate environment.

In this FAQ, Homejourney breaks down the key questions Singapore buyers ask about Fixed Rate vs Floating Rate Mortgage Which to Choose: Frequently Asked Questions, and connects you back to our main mortgage pillar guide Fixed vs Floating Rate Mortgage: Which to Choose in Singapore | Homejourney for deeper education and tools.

What is the difference between a fixed rate mortgage and a floating rate loan?

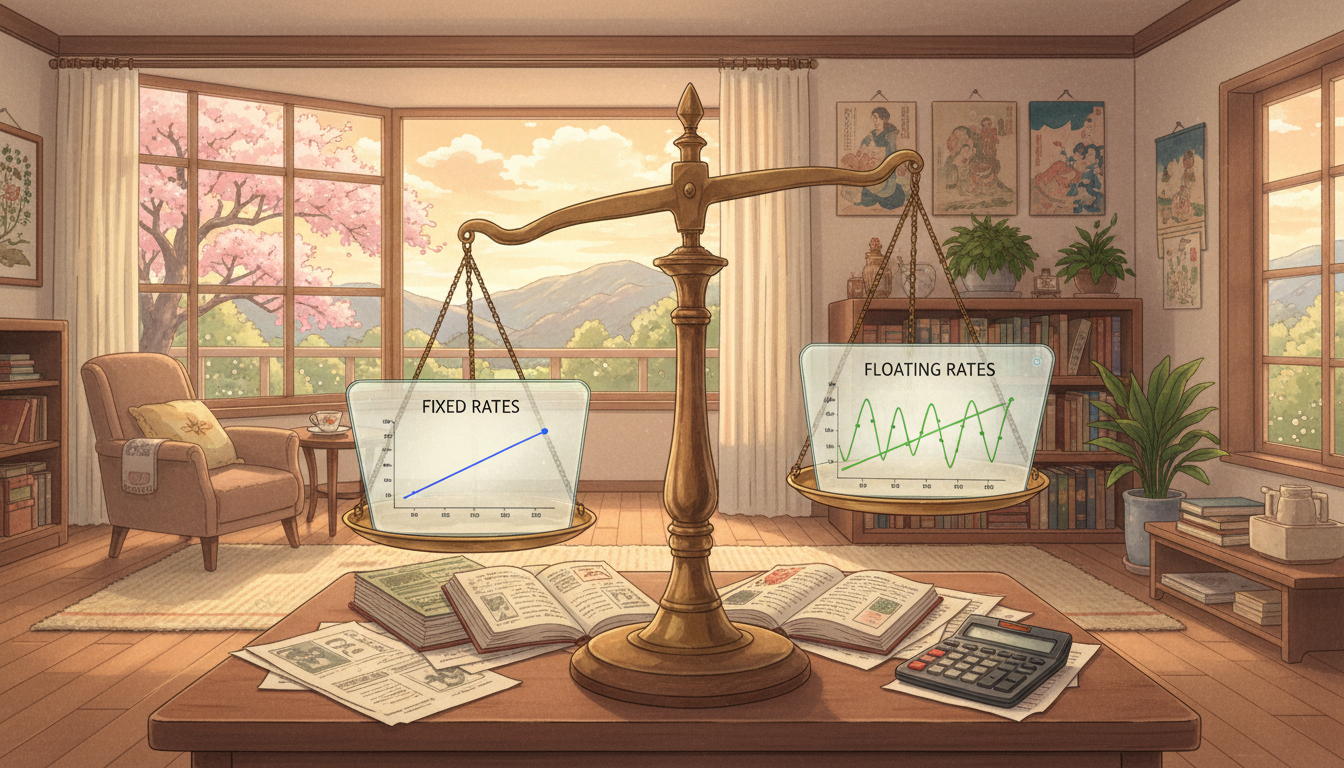

Fixed rate mortgage: Your interest rate is locked in for a set lock-in period (commonly 2–5 years in Singapore), so your monthly instalment stays the same during that period.

Floating rate loan: Your interest rate is pegged to a benchmark (today usually 3M or 6M SORA, or a bank’s board / fixed deposit rate), plus a bank spread, and can move up or down when the benchmark changes.[1][3]

In Singapore today, most new floating packages are SORA-pegged, where the formula typically looks like:

Floating rate = SORA (3M or 6M) + bank spread (margin).

Fixed rate packages from banks like DBS, OCBC, and UOB are usually slightly higher than the lowest floating packages because you are paying a premium for rate certainty.[1][3]

How are fixed and floating mortgage rates calculated in Singapore?

For fixed rate mortgages in Singapore:

- The bank sets a fixed interest rate (e.g. 1.70% p.a. for 3 years) for the agreed lock-in period.[2][3]

- After the lock-in, the loan usually converts to a floating package (often SORA or board-rate pegged) unless you reprice or refinance.

For floating rate loans, banks commonly use:

- SORA-pegged packages – e.g. 3M SORA + 0.60% bank spread.[1][2][3]

- Board rate – an internal rate set and revised by the bank.

- Fixed deposit rate-pegged (FDR) – pegged to the bank’s own fixed deposit rates for a specific tenor.[1]

Since MAS has transitioned away from SIBOR/SOR, new floating packages are primarily SORA-based, which reflects actual overnight interbank transactions in Singapore, making it more transparent and transaction-based.[1][3]

What is SORA and how does it affect my monthly payments?

SORA (Singapore Overnight Rate Average) is the volume-weighted average rate of unsecured overnight interbank transactions in Singapore, administered by MAS.[1][3] Banks commonly use compounded 3-month (3M) or 6‑month (6M) SORA as the reference for floating home loans.

3M vs 6M SORA:

- 3M SORA: resets every 3 months – your instalment adjusts more frequently, tracking market changes more closely.

- 6M SORA: resets every 6 months – slower to adjust, which can be good if rates are rising quickly, but slower to fall when rates drop.

Example (illustrative, not a quote):

Assume:

- Loan amount: S$600,000

- Tenure: 25 years

- Package: 3M SORA (1.20% p.a.) + 0.60% spread = 1.80% effective rate

At 1.80%, your monthly repayment is roughly S$2,486. If 3M SORA rises from 1.20% to 2.20%, your rate becomes 2.80% and your repayment jumps to around S$2,779 – about S$293 more per month. This volatility is the main trade-off for potential savings when SORA is low or trending down.[2][3]

Homejourney lets you track live 3M and 6M SORA and see how they move day by day on our bank rates page: Bank Rates .

How have fixed and floating rates moved recently in Singapore?

According to recent reporting, SORA has fallen from around 3% in early 2025 to about 1.2% by mid-December 2025, reaching a three‑year low as expectations for lower global rates built.[3] Fixed-rate packages have also come down and are "moving in tandem" with SORA-based floating rates.[3]

Banks such as OCBC observed that four in five new customers in 2025 still chose fixed packages, reflecting Singapore borrowers’ preference for stability even in a declining rate environment.[3] However, banks and market observers note that in a low or falling rate cycle, well-structured floating packages can generate meaningful interest savings for borrowers who can tolerate some volatility.[2][3]

For indicative current ranges (not offers):

- Recent fixed packages for first‑year rates on private properties have been seen around the mid‑1% range (e.g. 1.48%–1.70% p.a. for 2–3‑year fixed deals).[2]

- Promotional floating packages (e.g. 3M SORA + low spread) can be slightly lower than equivalent fixed packages, depending on the bank and lock‑in structure.[2][3]

For up‑to‑date and bank‑verified numbers, use Homejourney’s bank rate comparison with live data from DBS, OCBC, UOB, HSBC, Standard Chartered, Maybank, CIMB, RHB, and more: Bank Rates .

Fixed vs floating rate: what are the pros and cons?

Here is a quick mortgage rate comparison for Singapore borrowers.

Who should choose fixed rate vs who should choose floating rate?

From working with Singapore buyers across estates like Punggol, Sengkang, Tampines and condos in Bishan and Queenstown, there are clear patterns in which profiles tend to prefer which interest rate type.

Fixed rate may suit you if:

- You are a first‑time HDB buyer upgrading from rental at places like Yishun or Woodlands, and your monthly cash flow is tight.

- You have young children and value budgeting certainty (e.g. school fees, enrichment, childcare at Punggol or Bukit Batok).

- You are buying for own stay and plan to hold the property for at least 5–7 years.

- You are uncomfortable checking rates or adjusting your finances if instalments rise by a few hundred dollars a month.

Floating rate may suit you if:

- You are an investor buying a city‑fringe condo in areas like Geylang, Balestier or Bukit Merah and expect to review your financing every 2–3 years.

- You have strong, stable income and a buffer (e.g. 6–12 months of instalments in CPF OA or cash).