FHR Loans Explained: Homejourney's Complete FAQ Guide

A Fixed Deposit Pegged Home Loan (FHR loan) is a floating-rate mortgage where the interest rate is tied to a bank's fixed deposit (FD) rate plus a fixed spread, offering relative stability for Singapore homebuyers seeking predictable payments.

Homejourney prioritizes your safety by verifying rates from DBS, UOB, OCBC and more, helping you compare options transparently. This cluster article answers key questions on FHR loans (also called fixed deposit rate loans or FD pegged mortgages), linking back to our pillar guide on Fixed Deposit Pegged Home Loans Explained: FHR Guide by Homejourney ">Fixed Deposit Pegged Home Loans Explained: FHR Guide by Homejourney for full coverage.

What is a Fixed Deposit Pegged Home Loan?

An FHR loan pegs your home loan rate to the bank's fixed deposit interest rate for a specific period (e.g., 6 months), plus a bank spread. For example, if DBS FHR6 is 1.90% and the spread is 1.25%, your total rate is 3.15%.[1][2]

The 'FHR' stands for Fixed Deposit Home Rate, mainly offered by DBS and UOB. The number (e.g., FHR6, FHR9) indicates the FD tenure it's based on—longer tenures like FHR18 typically have higher base rates but smoother changes.[1][3]

Unlike fixed-rate loans, FHR rates aren't locked but tend to be steadier than market benchmarks, as banks balance FD payouts with lending costs.[1][2] Homejourney's bank rates page shows live FHR rates from all major banks for safe comparisons.

How Do FHR Loans Work in Practice?

Your total rate = FD benchmark rate + spread. The FD rate changes when banks update deposit rates, but banks notify you 30 days in advance per MAS rules.[6] Spreads are fixed during the loan tenure, often 0.75%-1.50% depending on the package.[1][3]

Real example: For a S$1 million HDB resale flat loan at 75% LTV (S$750,000), if FHR9 is 2.00% + 1.00% spread = 3.00% p.a., monthly repayment is about S$3,162 over 25 years (using standard formula).[3] Under TDSR (60% debt cap) and MSR (30% for HDB), ensure payments fit your income—use Homejourney's mortgage calculator for instant checks.

FHR loans suit under-construction properties with promotional low spreads (e.g., 0.50% pre-TOP, rising to 1.00% post-TOP).[3] CPF Ordinary Account funds at 2.5% p.a. can service payments, but you'll forgo OA interest.[4]

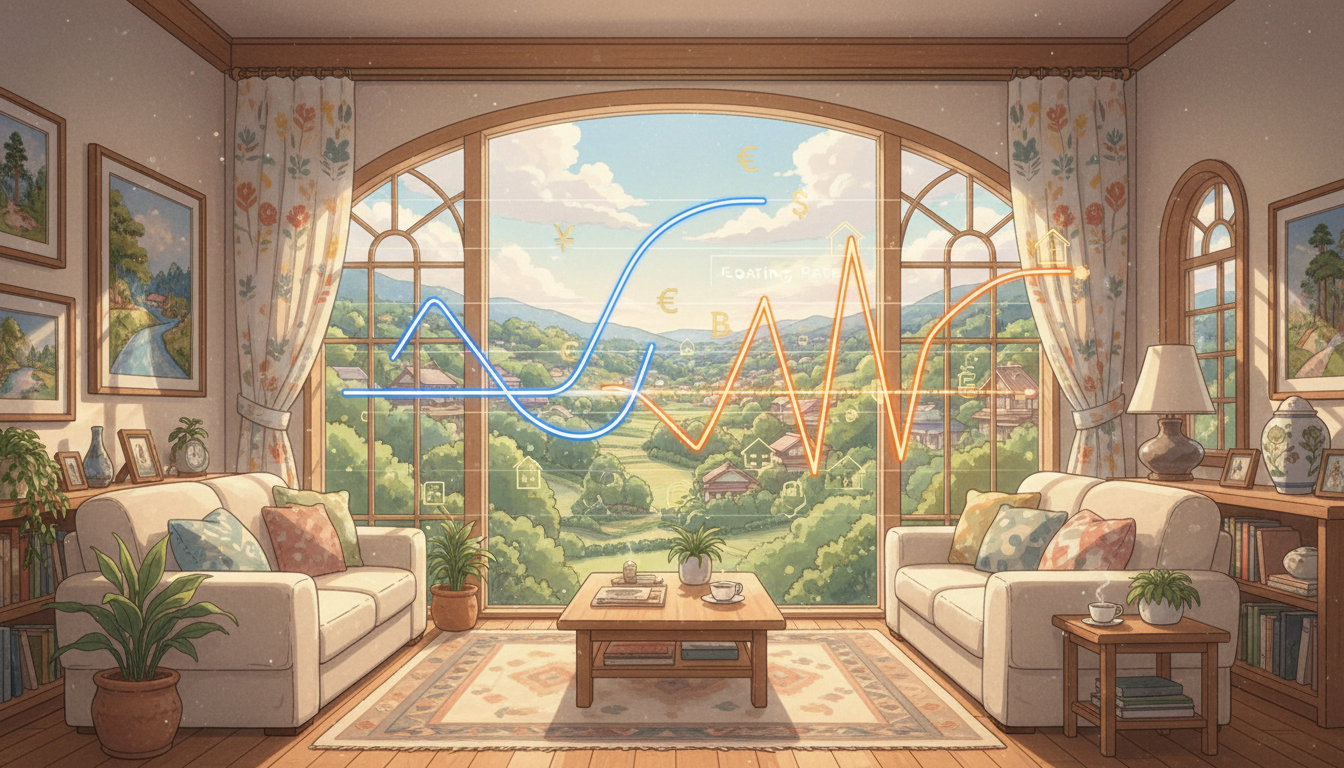

FHR vs SORA: Key Differences for Singapore Buyers

FHR is bank-controlled (tied to their FD rates), while SORA tracks actual interbank lending (3M compounded SORA at ~3.64% in early 2024).[2][4] FHR offers caps (e.g., 1.8% for 2 years) for protection, but banks can adjust FD rates freely.[2]

| Aspect | FHR Loan | SORA Loan |

|---|---|---|

| Peg | Bank FD rate | Market SORA |

| Stability | Smoother, bank-managed | Market-driven volatility |

| Current Appeal | Caps in high-rate era | Transparent, no bank discretion |

The chart below shows recent interest rate trends in Singapore:

As seen, FHR has lagged SORA rises, making it attractive now—but check Homejourney for latest from DBS, OCBC, UOB.[1][4] Learn more in our SORA Linked Home Loans Explained: Benefits of Applying via Homejourney ">SORA Linked Home Loans Explained.

Pros and Cons of FHR Loans

- Pros: Relative stability (less volatile than SORA), promotional caps, popular (90% of DBS loans in 2017).[1][3]

- Competitive in low-FD environments; zero-spread promos historically.[1]

- Cons: Bank discretion on FD rates (double-edged), higher long-term if spreads rise post-promo.[2]

- Not truly fixed—rates can increase; shorter tenures (FHR6) fluctuate more.[1]

For HDB buyers, compare with HDB loans (2.6% pegged to CPF OA +0.1%).[6] Private property investors: Factor ABSD (up to 65% for foreigners). Homejourney verifies eligibility instantly via Singpass.

Actionable Steps to Get an FHR Loan via Homejourney

- Check rates on Homejourney bank rates—compare DBS FHR6, UOB equivalents from HSBC, Standard Chartered, Maybank.

- Calculate affordability with our eligibility calculator (TDSR/MSR compliant).

- Apply via Singpass/MyInfo for multi-bank quotes—one form, offers from 10+ banks.

- Consult Homejourney Mortgage Brokers for personalized advice (free, no obligation).

- Search matching properties on Homejourney property search.

Disclaimer: Rates change; this isn't financial advice. Consult professionals. Data as of 2026 trends.[1][2][4]

Frequently Asked Questions on FHR Loans

1. Are FHR loans better than SORA in 2026?

Depends on outlook—FHR steadier short-term with caps, SORA more transparent long-term. Compare on Homejourney.[1][2]

2. Which banks offer FHR loans?

Mainly DBS (FHR6/9) and UOB; check OCBC, CIMB for similar FD-pegged. View all on Homejourney.[1][2]

3. Can I refinance to FHR?

Yes, if 2-3 years into current loan (lock-in penalties apply). Homejourney simplifies with multi-bank comparison.[3]

4. How does FHR affect CPF usage?

CPF OA can pay installments (lose 2.5% interest), with accrued interest refunded on full repayment.[4][6]

5. Is FHR suitable for first-time HDB buyers?

Yes for stability, but HDB loan cheaper if eligible. Use our calculator for MSR check.[6]

Ready to secure a stable rate loan? Start safely on Homejourney bank rates—compare FHR vs SORA today. For full details, read our pillar: Fixed Deposit Pegged Home Loans Explained: FHR Guide by Homejourney ">Fixed Deposit Pegged Home Loans Explained.