FHR Loans Explained: Fixed Deposit Pegged Home Loan FAQs | Homejourney

A Fixed Deposit Pegged Home Loan, also known as FHR loan, fixed deposit rate loan, FD pegged mortgage, or stable rate loan, ties your mortgage interest to a bank's fixed deposit (FD) rate plus a fixed spread.

This cluster article answers the most common questions Singapore home buyers ask about FHR loans, building on our pillar guide Types of Home Loans Singapore: Complete Comparison via Homejourney Types of Home Loans Singapore: Complete Comparison via Homejourney . At Homejourney, we prioritize your safety with verified rates from DBS, OCBC, UOB and more—compare them instantly at https://www.homejourney.sg/bank-rates.

What is a Fixed Deposit Pegged Home Loan (FHR)?

FHR stands for Fixed Home Rate or Fixed Deposit Home Rate, popularised by DBS Bank. It pegs your loan to the bank's published FD rate for a specific tenure (e.g., FHR6 for 6-month FD) plus a bank spread of 1.25%-1.5%.[1][2]

For example, if DBS FHR6 is 1.90% and spread is 1.25%, your total rate is 3.15%.[1] The FD component fluctuates with market conditions under MAS oversight, while the spread stays fixed.[2]

Unlike opaque board rates, FHR offers transparency as banks publish FD rates daily. DBS evolved from FHR18 (0.60%) to current FHR6 (around 1.4% as of late 2025).[1][2] Other banks like UOB offer similar FD-pegged packages.[1]

Homejourney verifies these rates in real-time. Use our bank rates page to see live FHR from DBS, OCBC, UOB, HSBC, Standard Chartered, Maybank, CIMB, and more.

How Does FHR Work in Practice?

Your total rate = FD Rate (e.g., DBS FHR6) + Spread. FD rates are influenced by MAS policy and tend to move slower than daily SORA, providing relative stability.[1][4]

Real Singapore example: For a $800,000 HDB resale flat in Tampines (under MSR/TDSR limits for a $10,000/month household), a 25-year FHR6 +1.3% loan at 2.7% means ~$3,500 monthly using CPF OA.[2] Post-TOP for new launches, spreads may rise slightly.[3]

Banks control spreads for profit, but zero-spread FHR promotions ended post-2017.[1] Track changes via Homejourney's eligibility calculator at https://www.homejourney.sg/bank-rates#calculator—auto-fills with Singpass for accurate TDSR checks.

FHR vs SORA: Key Differences for Singapore Buyers

FHR (FD pegged) offers steadier rates tied to bank deposits, less volatile than SORA (Singapore Overnight Rate Average), which follows daily money market fluctuations.[4]

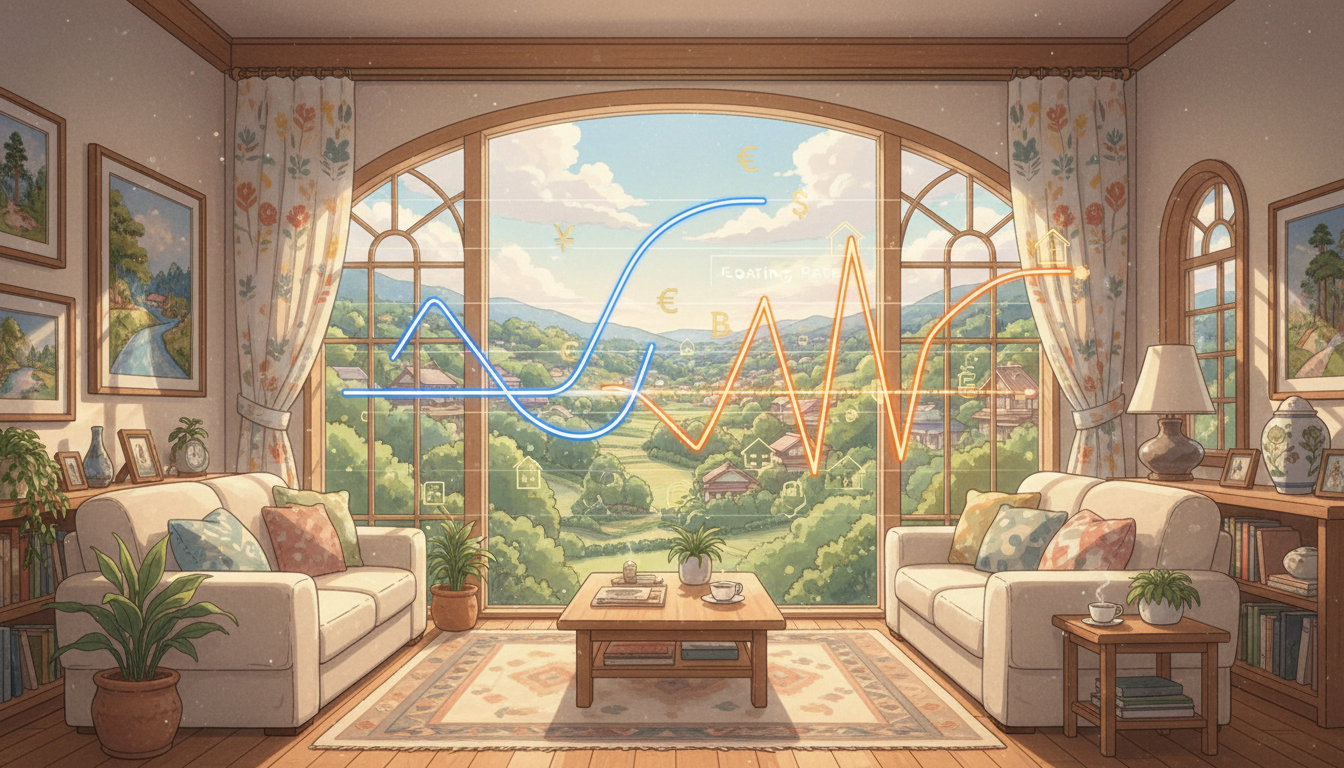

The chart below shows recent interest rate trends in Singapore:

As seen, FHR6 tracks FD rates closely, often 0.5-1% above 3M SORA but with fewer spikes—ideal for risk-averse first-time buyers financing HDB in areas like Punggol.[1][4]

| Aspect | FHR (FD Pegged) | SORA |

|---|---|---|

| Peg | Bank FD rate + spread | Daily compounded overnight rate |

| Volatility | Lower (semi-fixed) | Higher (market-driven) |

| Current Rate (2026 est.) | 2.7-3.2% | 2.5-3.0% |

| Best For | Stability seekers | Rate optimists |

Source: Bank data via Homejourney.[1][2][4] HDB loans (2.6% pegged to CPF OA +0.1%) remain cheapest for flats but cap at 75% LTV.[8]

Pros and Cons of Fixed Deposit Pegged Loans

- Pros: Transparent (published FD rates), relatively stable vs SORA, popular (90% DBS loans in 2017).[1] Lower short-term volatility suits budgeting for young families in Yishun BTOs.

- Stable for 6-18 months: Higher tenure FHR (e.g., FHR18) pays more but moves slower.[1]

- Cons: Still floating—rises with FD rates; banks adjust spreads post-TOP (e.g., 0.75% to 1%).[3] Not truly fixed like 2-3 year packages.

- Lock-in risks: 2-3 year penalties if refinancing early.

Insider tip: For HDB upgraders, pair FHR with CPF OA (2.5% interest) but monitor opportunity cost.[4] Homejourney's multi-bank application lets you submit once via Singpass to DBS, UOB, OCBC—get offers fast without shopping around.

Is FHR Right for You? Actionable Steps

- Check eligibility: Use Homejourney's calculator for MSR (HDB: 30% income) / TDSR (60% total debt).[Link to calculator]

- Compare rates: View FHR6 from DBS (1.4%+spread), UOB equivalents at https://www.homejourney.sg/bank-rates.

- Apply safely: One-click to multiple banks (HSBC, Maybank, CIMB, RHB)—Singpass verifies income/CPF instantly.

- Refinance tip: If SORA drops, switch via Homejourney's process. For properties, search budgets at https://www.homejourney.sg/search.

- Consult: Connect with Homejourney Mortgage Brokers for free, personalized advice.

Disclaimer: Rates as of Jan 2026; subject to MAS/HDB rules. Seek professional advice; Homejourney provides info, not financial advice.

Frequently Asked Questions: Fixed Deposit Pegged Home Loans

1. What banks offer FHR or FD pegged loans in Singapore?

DBS leads with FHR6; UOB, OCBC, HSBC, Standard Chartered offer similar. Compare all on Homejourney's verified bank rates page.[1][2]

2. Can I use CPF for FHR loans?

Yes, for HDB or private properties. CPF OA at 2.5% services payments, but you forgo interest. HDB loans are cheaper at 2.6%.[4][8]

3. FHR vs fixed-rate loan: Which is better?

FHR is floating but stable; true fixed locks rates 2-5 years. Choose FHR if expecting steady FD rates—see our Fixed Deposit Pegged Home Loans Explained: FHR Guide by Homejourney ">FHR Guide.[3]

4. How often does FHR change?

With bank FD revisions (monthly/quarterly), less frequent than daily SORA. DBS FHR tranches last ~18 months.[1]

5. Is FHR suitable for investors?

Yes for stable cash flow, but monitor ABSD/TDSR. Use Homejourney to match loans to investment properties in Projects Directory .

Ready to secure your Fixed Deposit Pegged Home Loan? Start with Homejourney's safe, transparent tools at https://www.homejourney.sg/bank-rates. Link back to our pillar: Types of Home Loans Singapore: Complete Comparison Types of Home Loans in Singapore: Complete Comparison | Homejourney for full insights.