FHR Loans Explained: FAQs on Fixed Deposit Pegged Home Loans | Homejourney

A Fixed Deposit Pegged Home Loan, also known as FHR loan, fixed deposit rate loan, or FD pegged mortgage, ties your mortgage interest to a bank's fixed deposit (FD) rates plus a fixed spread. This cluster article answers the most common questions Singapore home buyers ask about these stable rate loans, helping you decide if it's right for your HDB flat or private condo purchase.

Homejourney prioritizes your safety by verifying rates from DBS, OCBC, UOB and more, so you can compare confidently without hidden fees. For our full pillar guide, see Fixed Deposit Pegged Home Loan Explained: FHR Guide by Homejourney ">Fixed Deposit Pegged Home Loan Explained: FHR Guide by Homejourney.

What is a Fixed Deposit Pegged Home Loan (FHR)?

FHR stands for Fixed Deposit Home Rate, offered mainly by DBS and UOB in Singapore. Your loan rate = bank's FD rate (e.g., FHR6 for 6-month average) + bank spread (e.g., 1.25%). For example, if DBS FHR6 is 1.90% and spread is 1.25%, your total rate is 3.15%.[1][2]

The number in FHR (like FHR6, FHR9, FHR18) shows the FD tenure it's pegged to—higher numbers mean steadier but often higher base rates. Banks update FD rates periodically, so your mortgage adjusts, but less volatile than daily benchmarks.[1][3]

Unlike HDB's fixed 2.6% concessionary rate (0.1% above CPF OA at 2.5%), FHR is a bank loan for both HDB and private properties. Use CPF OA for repayments via CPF portal, but note the 2.5% opportunity cost.[5][6]

How Does FHR Work in Practice?

Banks publish FD rates publicly, pegging loans to a specific tranche. DBS simplified to FHR6 recently; previously FHR18 or FHR9. If FD rates rise (e.g., due to market conditions), your loan rate follows after 30 days' notice per MAS rules.[1][7]

Key Singapore rules apply: TDSR caps repayments at 55% of income; MSR at 30% for HDB. For a $800,000 HDB resale, with 20% downpayment ($160,000 via CPF/cash), you'd finance $640,000. At 3.15% over 25 years, monthly repayment ~$3,100—check if under TDSR using Homejourney's mortgage calculator.[6]

Lock-in periods (2-3 years) prevent early refinancing; caps (e.g., 1.8% for 2 years) limit rises. Post-TOP for new launches, spreads may rise from 0.8% to 1%.[3]

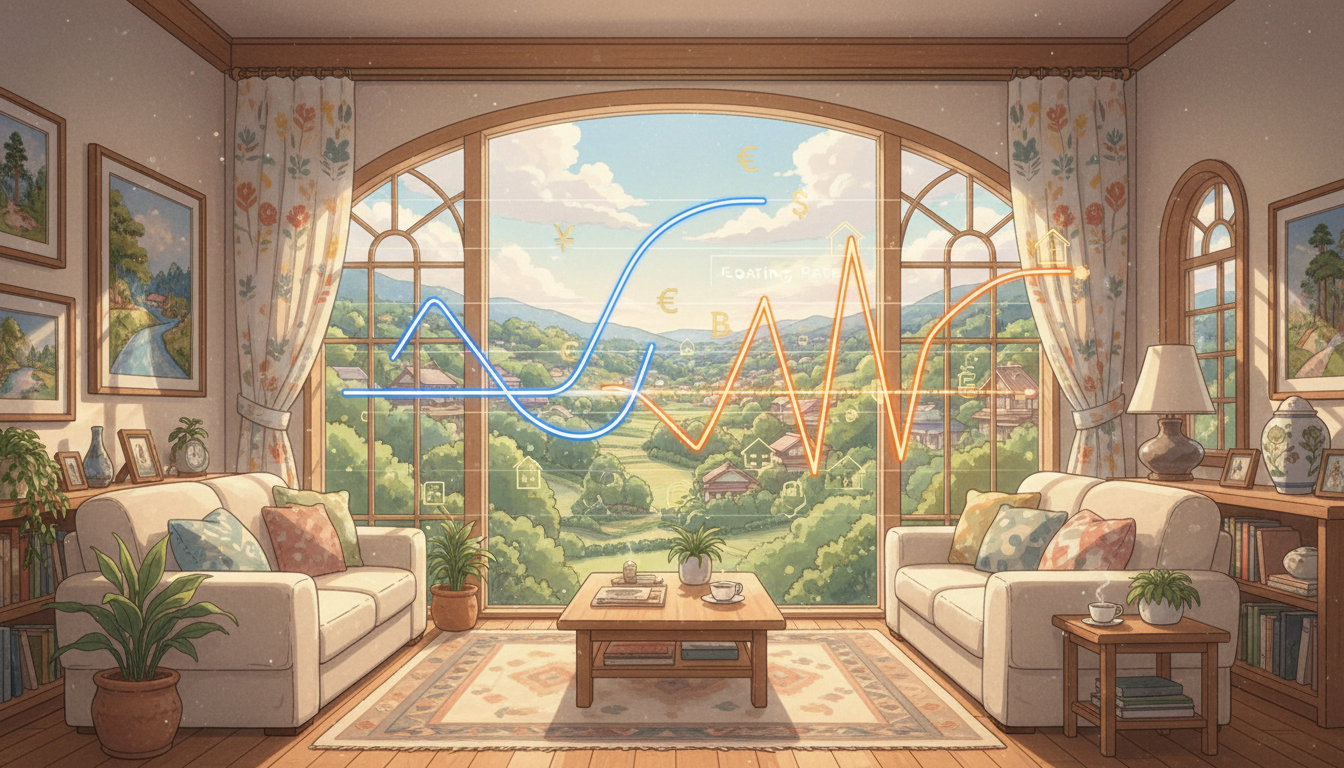

The chart below shows recent interest rate trends in Singapore:

As seen, FD rates track broader trends but smoother than SORA spikes.[1][5]

FHR vs SORA: Which is Better for Singapore Buyers?

FHR vs SORA: SORA (Singapore Overnight Rate Average) is a floating benchmark published daily by ABS, compounded over 3/6 months—now ~3.64% (Feb 2024 data, check live on Homejourney).[5] FHR uses bank's FD rates, often lower volatility as banks pay depositors similarly.[1][2]

| Feature | FHR (FD Pegged) | SORA |

|---|---|---|

| Peg | Bank FD rate + spread | Market SORA + spread |

| Volatility | Lower, bank-controlled | Higher, market-driven |

| Current Appeal | Stable in rising rates | Potentially lower if SORA falls |

FHR suits risk-averse buyers (90% DBS uptake in 2017); SORA for those expecting rate cuts. Compare live rates from DBS, OCBC, UOB, HSBC on Homejourney's bank rates page.[1][5]

Pros and Cons of FHR Loans

- Pros: Predictable—FD rates rise slower; often low spreads (1-1.5%); caps for peace of mind.[1][3]

- Popular for under-construction properties (lower pre-TOP spreads).[3]

- Cons: Bank sets FD rate (could rise without market force); not truly fixed—adjusts with FD changes; higher long-term if spreads lock high.[2]

- No zero-spread promos now; refinance risk post-lock-in.[1]

Insider tip: For HDB upgraders in areas like Punggol, pair FHR with CPF for downpayment (up to 25% LTV limit). Always verify TDSR via Homejourney calculator before committing.[6]

Actionable Steps to Get an FHR Loan on Homejourney

- Check eligibility: Use Homejourney mortgage calculator with income/CPF data via Singpass.

- Compare rates: View DBS FHR6, UOB equivalents vs SORA from all banks on bank-rates.

- Apply multi-bank: One-click submission via Singpass/MyInfo—get offers from DBS, OCBC, UOB, HSBC, Standard Chartered, Maybank.

- Refinance if needed: Track via Homejourney; connect with our mortgage brokers for free guidance.

- Search properties: Find HDB/condos in budget at Homejourney property search.

Disclaimer: Rates change; this is not financial advice. Consult professionals; Homejourney verifies data for trust.[7]

Frequently Asked Questions on Fixed Deposit Pegged Home Loans

Q1: Are FHR loans fixed or floating?

FHR are floating—pegged to changing FD rates + fixed spread, unlike true fixed-rate loans. Expect 30-day notice for changes.[1][7]

Q2: Which banks offer FHR in 2026?

Primarily DBS (FHR6) and UOB; others like OCBC may have FD-pegged variants. Compare all on Homejourney bank-rates.[1][2]

Q3: Can I use CPF for FHR repayments?

Yes, for HDB or private properties. Submit via CPF site; capped by withdrawal limits (e.g., 80% of valuation for first property).[5][6]

Q4: FHR vs HDB loan—which for first-timers?

HDB at 2.6% for flats only; FHR competitive for private/HDB resale if rates low. See HDB贷款vs银行贷款2026年最新对比:Homejourney指南 ">HDB vs Bank Loan Comparison.[6]

Q5: How to switch to FHR if rates drop?

Post-lock-in, refinance via Homejourney's multi-bank app—Singpass speeds approval. Track SORA/FD trends on our platform.

Ready to secure a safe FHR loan? Start at Homejourney bank-rates for verified comparisons and easy applications. Trust Homejourney for transparent property journeys—your safety first.