Board Rate Home Loans Pros and Cons: Bank Rate Comparison Guide

Board rate home loans, also known as internal board rate or bank board rate mortgages, peg interest to a bank's internal fixed deposit rate plus a spread, offering stability for Singapore homebuyers seeking predictable payments.

Homejourney prioritizes your safety by verifying real-time rates from DBS, OCBC, UOB, and more, helping you compare board rate loans confidently without hidden risks.

What Are Board Rate Home Loans?

A board rate loan ties your mortgage interest to the bank's internal board rate—typically linked to its fixed deposit (FD) rates—plus a margin set by the bank. Unlike SORA-linked loans that follow market benchmarks, board rates give banks discretion to adjust based on their funding costs.

This makes board rate loans appealing for short-term stability, especially amid 2026's falling rates where 3M SORA hit 1.2% lows.[5] However, they carry board rate risks like opaque changes at the bank's whim.[3]

For context, this cluster dives into board rate specifics, linking back to our pillar guide on Singapore Home Loans 2026: Complete Comparison for broader mortgage education.

Board Rate Home Loans Pros and Cons

Pros of Board Rate Loans

- Stability in volatile markets: Rates often stay lower longer than SORA during rate hikes, as banks smooth FD adjustments.[3]

- Higher approval odds: Banks favor board rates for riskier profiles, boosting chances for HDB upgraders or investors. See our related article: Board Rate Home Loans Pros & Cons: Boost Approval Odds | Homejourney

- Competitive packages: Paired with cash rebates (e.g., $2,000-$2,800 for refinancers on loans over $500k).[1]

- Flexibility for big loans: Best for $1M+ properties with tiered low rates unpublished online.[2]

Cons and Board Rate Risks

- Lack of transparency: Banks can hike board rates without notice, unlike public SORA.[8]

- Higher long-term costs: Post-lock-in, spreads widen (e.g., 3M SORA +1.00%).[1]

- Penalty traps: 2-3 year lock-ins with fees for early exit, riskier vs. SORA's free conversions.[2]

- Less competitive now: With SORA at 1.34%, board rates lag for HDB switchers saving $4,100 yearly on $500k loans.[5]

Compare board rate vs SORA on Homejourney's real-time tool at https://www.homejourney.sg/bank-rates to see which fits your profile.

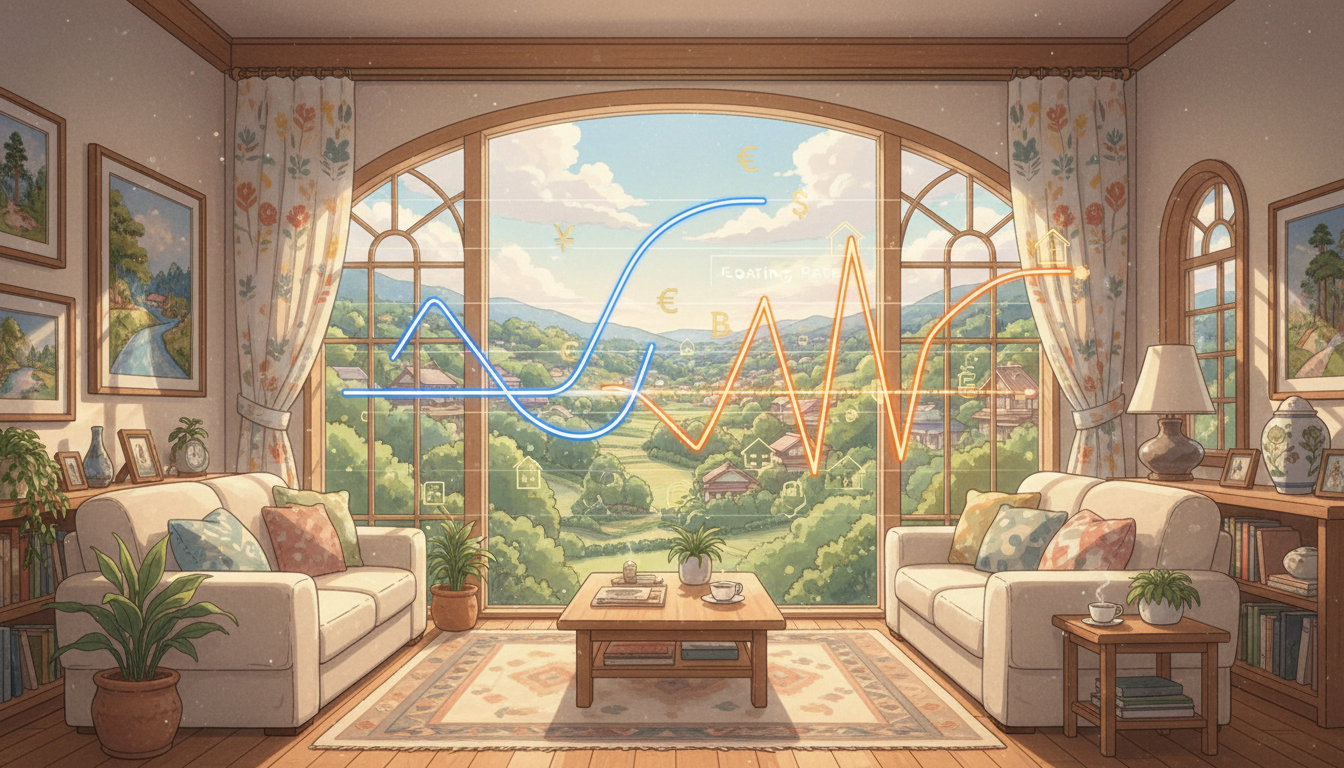

Board Rate vs SORA: Key Differences

Board rates offer bank-controlled stability but expose you to internal rate mortgage unpredictability, while SORA follows transparent 3M compounded averages (now ~1.3-1.4%).[6] Board suits conservative buyers; SORA favors rate watchers.

The chart below shows recent interest rate trends in Singapore:

As seen, SORA's drop from 3% to 1.2% makes floating loans attractive, but board rates provide a buffer if hikes return mid-2026.[5]

Singapore Bank Board Rate Comparison 2026

Homejourney verifies rates from partner banks for safe decisions. Current packages (as of Jan 2026; check https://www.homejourney.sg/bank-rates for updates):

| Bank | Year 1-2 Rate | Post-Lock-In | Min Loan | Rebate (Refi) |

|---|---|---|---|---|

| DBS | 1.50-1.78% Fixed | 3M SORA +1.00% | $500k-$700k | $2,000-$2,800[1] |

| OCBC | 1.60% Fixed | 3M SORA +0.50% | $400k | $2,000-$2,800[2] |

| UOB | 1.50% Fixed (3yr) | 3M SORA +1.00% | $500k | $2,000[2] |

| HSBC/Standard Chartered | 1.35-1.50%* (Tiered) | 3M SORA +0.60-1.00% | $500k-$2M | $2,300[2] |

| Maybank/CIMB/RHB | 1.35%* Fixed | Board + Spread | $1M+ | Varies[2] |

*Conditions apply for high-value loans. Use Homejourney's calculator at https://www.homejourney.sg/bank-rates#calculator for personalized rates including TDSR limits.

Actionable Steps: Choosing Board Rate Loans

- Assess eligibility: Input income/debt into Homejourney's tool—Singpass auto-fills for speed.

- Compare banks: View DBS vs OCBC board rates live; apply to multiples with one form.

- Time refinancing: Switch from HDB's 2.6% if bank rates <2%—save thousands yearly.[5]

- Mitigate risks: Opt for free conversion clauses; track via Homejourney.

- Apply safely: Use our multi-bank system—banks compete for you. Link properties in budget at https://www.homejourney.sg/search.

DBS shines for HDB loans with 13x uptake surge; OCBC for rebates.[5] Always consult pros—Homejourney connects you to mortgage brokers.

Homejourney: Your Trusted Partner

At Homejourney, user safety comes first—we verify rates, enable Singpass applications, and let banks bid for your loan. Track SORA vs board live, avoiding pitfalls in our transparent platform.

Refinancers: HDB owners saved up to $4,100 annually switching.[5] Explore projects at Projects or maintenance like Aircon Services .

FAQ: Board Rate Home Loans Singapore

Q1: Are board rate loans better than SORA in 2026?

A: Board offers stability but higher risks; SORA is cheaper now (1.34%). Compare on Homejourney. Related: SORA Home Loans 2026: Bank Rates Comparison Guide | Homejourney

Q2: What are current DBS board rates?

A: 1.50% fixed Y1-2, then 3M SORA +1.00% (min $500k).[1] Verify at https://www.homejourney.sg/bank-rates.

Q3: Can I switch from board rate easily?

A: Check lock-ins (2-3yrs); many offer waivers on sale.[1] Use our refinancing guide.

Q4: Board rate risks for first-time buyers?

A: Potential hikes; prefer SORA for transparency. Boost approval with board: Board Rate Home Loans Pros & Cons: Boost Approval Odds | Homejourney

Q5: How to apply via Homejourney?

A: One form, multi-bank offers, Singpass integration—faster, safer.

Disclaimer: Rates fluctuate; not financial advice. Consult advisors. Data from MAS/HDB-aligned sources.[4][5]

Ready to compare Board Rate Home Loans Pros and Cons: Bank Rate Comparison Guide? Start at https://www.homejourney.sg/bank-rates and link back to our pillar for full insights.

References

- Singapore Property Market Analysis 5 (2026)

- Singapore Property Market Analysis 3 (2026)

- Singapore Property Market Analysis 1 (2026)

- Singapore Property Market Analysis 2 (2026)

- Singapore Property Market Analysis 8 (2026)

- Singapore Property Market Analysis 6 (2026)

- Singapore Property Market Analysis 4 (2026)